Hunterbrook Media’s investment affiliate, Hunterbrook Capital, has no positions related to this article at the time of publication. Positions may change at any time. Our contributor has made extensive filings with the SEC and FINRA for potential securities fraud and anti-touting violations. If you’re an affected investor or former employee of any of these companies and want to tell us about it, write ideas@hntrbrk.com.

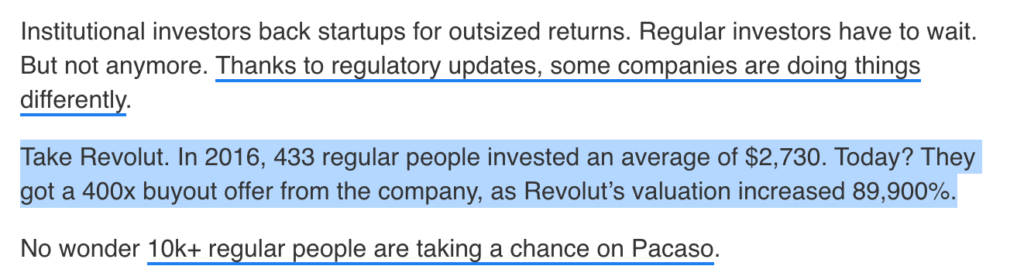

In 2012, Congress and the Securities and Exchange Commission passed a law that would open the doors to equity crowdfunding. The JOBS Act passed in 2012. A lengthy period of rule finalization then followed, with the first crowdfunding investments to the general public under this legislation occurring in 2016. For the first time, buying shares in private startups wasn’t just for the wealthy and financially sophisticated. Restrictions designed to protect amateur investors were relaxed as part of a mission to “democratize” finance. No longer would ordinary people be forced to watch from the sidelines as the next SpaceX or Instagram rocketed to the moon.

Or so the sales pitches went. What actually followed was exactly what skeptics predicted: a parade of failing companies raising hundreds of millions from unsuspecting investors through campaigns built on misdirection and deceit. Success stories proved rare. Disasters became routine.

A Hunterbrook Media investigation reveals how a network of distressed startups, a hungry marketing firm, and some of America’s most trusted financial media brands — wittingly or not — ended up separating small investors from their money. A remarkable number of respected outlets, from blue-chip financial newsletters to The Wall Street Journal, appear to have hosted misleading or downright false ads, calling into question their due diligence and adherence to disclosure obligations. The result looks like an unhappy masquerade: troubled companies partnering with slick marketers to hide their rotten balance sheets behind the prestige of reputable mastheads, and news outlets indirectly promoting the very companies they should have been scrutinizing.

The little guy finally had his seat at the table. The game was rigged.

By following the trail from the narrative factory to the newsletter inbox, a clear pattern emerges of how these companies manufactured the appearance of success to mask the reality of failure.

Here’s how it worked:

- Manufacturing the pitch. DealMaker Marketing Services Formerly known as DealMaker Reach. Its legal entity name is still DealMaker Reach, LLC. , an arm of financial firm DealMaker, collected fat fees for helping early-stage companies — including Boxabl, HeartSciences, EnergyX, M2i Global, Pacaso, RAD Intel, and Miso Robotics — craft ads and landing pages that stretched the truth, sometimes beyond the breaking point.

- ‘Trust-washing’ These ads appeared in premium slots in newsletters with millions of subscribers — like Morning Brew, Robinhood’s Sherwood News, and The Wall Street Journal’s 10-Point.

- Last ones in the pool. While readers were frequently told that they’d be investing alongside venture capital firms and other financial professionals, these companies largely turned to retail investors after deteriorating circumstances forced their hands. The amateurs essentially bailed out the pros, buying heavily-restricted shares at jaw-dropping and opaque valuations.

While we’re publishing now to call attention to the scale of the problem, we believe we’ve captured here only a fraction of all concerning cases. In our review of additional examples, we struggled to find any that didn’t exhibit similar concerns.

Sign Up

Breaking News & Investigations.

Right to Your Inbox.

No Paywalls.

No Ads.

Pay-to-Print Coverage

Hunterbrook approached all eight media outlets named here for comment. Only two replied. Their statements are included below.

Intermediaries like DealMaker didn’t — and couldn’t — pull this off alone. Instagram ads and landing pages can only go so far. Media legitimization is crucial.

Say you’re reading your morning newsletter from a trusted source. There’s a section titled “Presented By” that otherwise looks the same as the rest. Is this an ad? Who wrote it? At the least you might assume that the outlet in question did meaningful due diligence on your behalf — as some of them claim to do.

Few outlets count on this simple trust more than Morning Brew. A hotshot daily newsletter network with over 4 million claimed subscribers, its rapid rise led to an acquisition by publishing giant Axel Springer, parent company of both Politico and Business Insider. Hunterbrook’s analysis found that Morning Brew ran these crowdfunding ads in 165 editions of their flagship newsletter in 2025 alone. This may be an undercount. Morning Brew can send different ads to different subscribers. Hunterbook’s count is based on Morning Brew’s 2025 archives, which only capture one version of each edition. It also continued to run them regularly even after we approached for comment — to which we still have yet to receive a reply.

But it wasn’t just them. We found dozens of concerning examples across newsletters from Sherwood News (operated by a subsidiary of investment company Robinhood), The Wall Street Journal, 1440 (over 4.6 million claimed subscribers), TLDR (1.6 million) and Tangle News (460,000).

Tangle, an independent publication, provided Hunterbrook with a long and earnest response. Its founder affirmed that it did conduct both internal and referral-based due diligence. This doesn’t appear to have extended to comparing the provided ad copy to issuers’ disclosure documents. Tangle is reviewing its policies.

Benzinga, which boasts about 25 million monthly readers, went even further with a promotional post, seemingly presented as its own independent research, that was mostly just the fundraising company’s marketing boilerplate. The original Benzinga post contained a link to its Advertiser Disclosure policy in its header. Said policy, which can be viewed before it was updated here, stated that “the opinions expressed here are our own and are not influenced by any advertiser or affiliate partnership.” After Hunterbrook’s reach-out, Benzinga expanded the language of this policy without adjusting its listed effective date. Exec Sum, a financial newsletter run by Twitter/X personality Litquidity, did the same for its more than 350,000 subscribers.

In response to a request for comment, Benzinga shared the following statement: “We value Hunterbrook’s reporting on a variety of investigative topics like insider trading and other financial improprieties. We always endeavor to improve practices in conjunction with our legal teams, regulators, issuer clients, and general public inquiries.”

The effect of this legitimatization is evident in the numbers: Of the $75 million that startup EnergyX raised in 2024, DealMaker attributed “over $50 million” to these sponsored ads.

The pitches tended to follow a common theme: making small investors feel like they were joining something larger than just an investment. In a panel interview with DealMaker’s CEO and three fundraising founders, Morning Brew’s cofounder Alex Lieberman waxed poetic on this point:

“There are a lot of times where the word community is used but it isn’t necessarily authentic community,” he said. “Making retail investors part of your community, via investment in your business, [that] is the purest form.”

Two Truths and Some Lies

Note: We’ve included three short explainer sections as an investing and legal crash course. Seasoned market players can skip down to the deal profiles.

There are two classic ways to raise money: sell a better mousetrap or tell a better story. But what happens when you only have the story — and it’s not an especially good one? What if growth has stalled, losses have piled up, and professional investors have pulled back?

It’s no crime to fail in business. Startups should try hard things, with informed investors buying as much risk as they can stomach. What matters is what companies do after things go awry. If they turn to retail investors for a bailout, what story do they tell them?

We found that these companies’ legal disclosure filings were largely honest and typically painted a bleak picture of their position and prospects. But placed between investors and these unwieldy documents were layers of ads and landing pages — written in plain English, with far rosier outlooks, and, sometimes, outright falsehoods.

Regulatory Primer

U.S. securities law divides investors into two classes:

- Accredited investors, who meet special criteria around wealth, income, and financial licenses. The government assumes they have more investing experience, along with more loss cushion.

- Non-accredited (“retail”) investors, who may individually have deep financial expertise, but who on aggregate are considered a class worth protecting from potentially predatory deals.

In light of historical grift, the government has long restricted non-accredited investors from buying certain securities — like penny stocks and most private company shares — without special waivers or certifications. Uncle Sam prefers at least some guardrails.

The JOBS Act, passed in 2012, partially reversed this trend by permitting companies to directly approach retail investors with Kickstarter-style campaigns Unlike KickStarter, DealMaker’s platform doesn’t allow investors to browse between multiple investment offers. Each offering is hosted individually on its own DealMaker microsite. offering shares instead of early products. This legislation — including later amendments — gave companies two new options to mix-and-match:

- Regulation CF campaigns can raise up to $5 million per rolling year

- Regulation A+ campaigns can go as high as $75 million per rolling year There are two tiers for Regulation A+ fundraising. Tier 1 only accounts for around 5% of dollars raised, as it has a lower cap of $20 million per rolling year and is subject to compliance laws for each individual state that the securities are offered in. Our focus here is on Tier 2 campaigns, which preempt state regulation in favor of the SEC alone.

Because these campaigns target less affluent and sophisticated audiences (who can invest up to certain caps), the ads that issuers and their paid partners may run for these campaigns are subject to disclosure requirements and other restrictions:

- Ads for offerings made pursuant to Reg CF give the issuer a choice: They can either provide the details of the offering, but then only extremely limited factual details about the company and its business; or they can describe the business, but not the specific terms of the offering.

- Though Reg A+ campaign ads may include sales copy alongside offering terms, they are of course subject to general anti-fraud rules, such as Section 17(a) of the Securities Act, which prohibits “obtaining money or property” by means of false or misleading statements.

- Under either program, the content must make clear that it is a paid promotion, and, according to at least one lawyer we spoke to, must also include the amount of compensation received.

Dozens of the ads we reviewed for this investigation seemingly failed to follow the first and second rules, and, while most contained some marker identifying them as paid content, the level of clarity of those disclosures varied widely. And no ads disclosed the specific compensation received for their placement.

Brenda Hamilton, a securities lawyer and founder of Hamilton & Associates Law, described this shortcoming to Hunterbrook bluntly: “The public is entitled to know the information was bought and paid for and for how much.”

A Scorecard

To illustrate what these investors were truly buying, each deal profile covers a few key metrics.

- Revenues

Did the company have meaningful paying customers yet?

While startups are often unprofitable in their early days, it’s important to know if they’re actually serving customers at all. Many of these marketing campaigns relied heavily on projections, obscuring multiple years of operations with little or zero sales traction.

- Book Value

How much was the company worth on paper?

Accountants use the term “net tangible book value” to capture what a company’s hard assets are worth, minus all its financial liabilities. While this is always an incomplete picture — as it doesn’t factor expected growth — it provides a useful baseline.

- Offered Valuation

What true price were new investors buying in at?

The SEC doesn’t require these companies to give investors a straight answer here. While their full legal disclosures must provide the raw inputs, investors are left to do the math themselves. This is difficult given the complexities and inconsistencies of filings. Hunterbrook has deferred to estimates from crowdfunding aggregator Kingscrowd, which itself notes that its estimates “can be inaccurate and may indicate a lack of transparency from the company.” This number is far more crucial than the offered price per share, as comparing a company’s offered valuation to its book value uncovers how much of a markup investors are paying for uncertain growth.

While infant startups still building their foundations can reasonably charge substantial markups, higher multiples become harder to justify with each passing year that a company burns cash without getting closer to that growth materializing — or, as in some cases here, after revenues fall sharply.

Deal Profiles

Each of the deal profiles below proceeds in three sections — first, we provide our scorecard metrics; second, we describe the company and the content of its crowdfunding ads; third, we identify examples of false or misleading claims made either in those ads or related marketing materials. Hunterbrook approached all seven featured companies regarding its findings. Only one replied. Its comments have been included below.

Methodology: All book values were calculated as of the start of each company’s 2025 financial year. As none are turning a net profit, these figures largely reflect the cash they’ve accumulated from investors. The listed offered valuations are pre-money and don’t factor bonus shares.

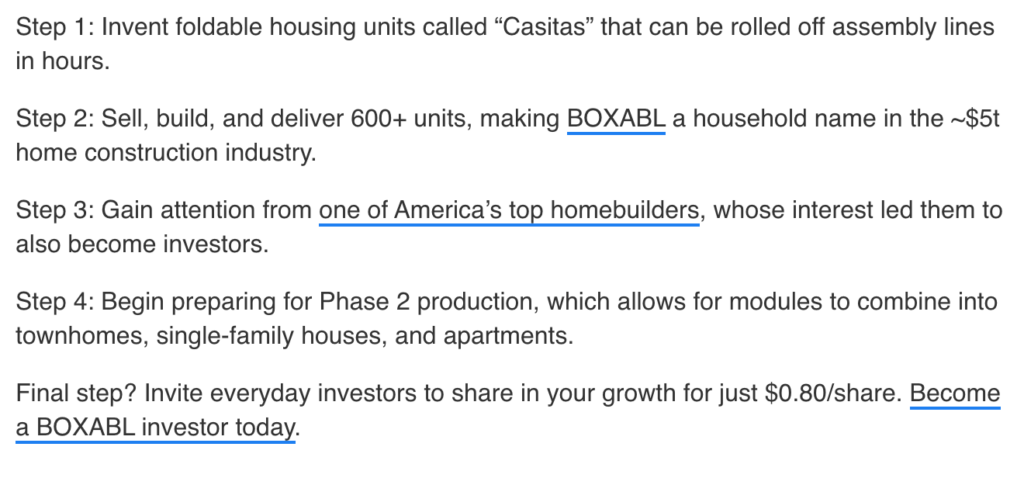

#1 – Boxabl

Stats: 2024 Revenues: $3.4 million. Book Value: $52.6 million. Offered Valuation: $3.5 billion. Markup: 66.6x.

Boxabl makes modular homes that can be collapsed for shipping like hulking IKEA boxes. The company claims to build each base-model Casita in “nearly four hours” using its “advanced assembly line” system, and boasts a reservation list of more than 190,000.

The company’s legal filings, however, tell a less optimistic story. Only 7,732 of those deposits are backed by cash deposits of any size, As of Boxabl’s last quarterly report, filed Nov. 14, 2025. and few depositors have ever actually completed a purchase. Boxabl sold just eight Casitas over the first nine months of 2025, all while writing off an additional 68 of its hundreds of stuck inventory units as either too damaged or now obsolete.

The company’s early operations also ran into a critical snag: It hadn’t secured required state approvals. Even today it can only deliver standalone units to 15 states Boxabl lists varying numbers here in different places. The FAQ section of its current website only names three states — California, Nevada, and New Mexico — where a Casita can be purchased without planning approval from a local building department. , some of which require further local permissions.

The company nonetheless still plans to go public via a SPAC merger at a $3.5 billion valuation.

Concern #1

- Claim: Boxabl sold recent investors on a “first of its kind” 2022 partnership with homebuilding giant D.R. Horton, which allegedly included a “phase 1 order for 100 Casitas.”

- Reality: No Boxabl SEC filings reviewed by Hunterbrook have listed D.R. Horton as a delivery recipient. As a Hunterbrook analysis only identified 15 total units shipped to unlisted buyers, this order appears to have been either cancelled or heavily trimmed. Hunterbrook asked D.R. Horton to clarify and didn’t receive a response. As this order was announced four years ago and Boxabl has struggled to sell its excess inventory, a mere fulfillment delay seems unlikely. And not for lack of inventory, as over 60% of Boxabl’s built homes remain unsold.

Concern #2

- Claim: Potential investors were told that Boxabl had delivered over 600 units by early 2025.

- Reality: According to its own SEC filings, through Nov. 10, 2025, Boxabl had delivered only 293, of which 207 went to two early buyers in 2022.

#2 – HeartSciences

Stats: 2024 Revenues: $4,000. These issuers report results on a delayed basis and in some cases use non-calendar reporting years. These particular results are for HeartScience’s latest reported fiscal year, which ended April 30, 2025. Book Value: -$1.4 million. Offered Valuation: $5.0 million. Markup: ∞.

HeartSciences ($HSCS) has partnered with multiple hospital research teams to bring AI into the business of ECG heart readings. The company was founded in 2007 and has yet to commercialize its technology.

When will it finally go to market? Despite telling investors as late as September 2025 that it was still targeting initial FDA approval “this year,” it had yet to even file its application when those statements were made. It only did so in mid-December, months too late for a possible 2025 approval.

Concern #1

- Claim: “Wall Street just raised its price target. Some analysts were projecting a $14 one-year share price target for HeartSciences (Nasdaq: HSCS). Now, they think it’ll hit $15.”

- Reality: HeartSciences’s website lists three analysts that cover its stock. All three work for firms that have had financial relationships with the company. Of 12,135 Wall Street analysts evaluated for their prediction quality, the trio rank 11,978th, 12,068th, and 12,066th. Also, none of them raised their target to $15 as claimed. That was an old evaluation, which had been downgraded five months before this ad went out.

Concern #2

- Claim: “With one-year price targets as high as $14, buying our investment unit for $3.50 gives you over 500% upside potential at that target.”

- Reality: Beyond the controversial nature of the target-setting, this math includes a basic error: At a $14 share price, the potential net return (factoring the included warrant) was about half of the quoted 500%. Though this is also academic, as the alluded-to analyst has since trimmed his target to $9.20 — which is still more than three times higher than the stock’s current trading price.

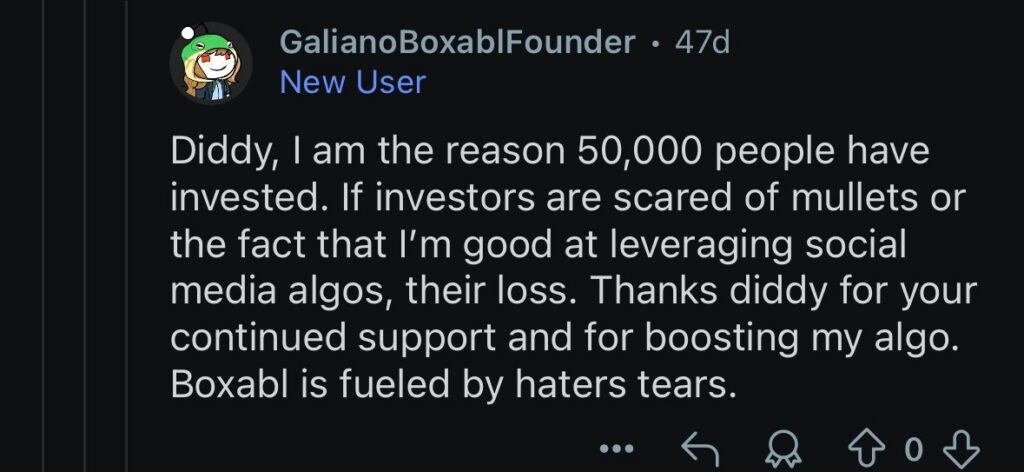

#3 – RAD Intel

Stats: 2024 Revenues: $1.2 million. Book Value: -$1.8 million. Offered Valuation: $149.7 million. Markup: ∞.

RAD Intel, “the ChatGPT of marketing,” spent $2.9 million on its own sales and marketing in 2024. The payoff? About $1 million in revenue over the first half of 2025 — on which it lost $6.2 million. The company operates without a permanent office and appears to make most of its money from selling shares to new investors.

Up to $11.8 million of its current fundraising will go to cashing out existing shareholders, including significant holdings from the company’s CEO, president, and board of directors.

(Captured from Morning Brew’s Nov. 10, 2025 edition.)

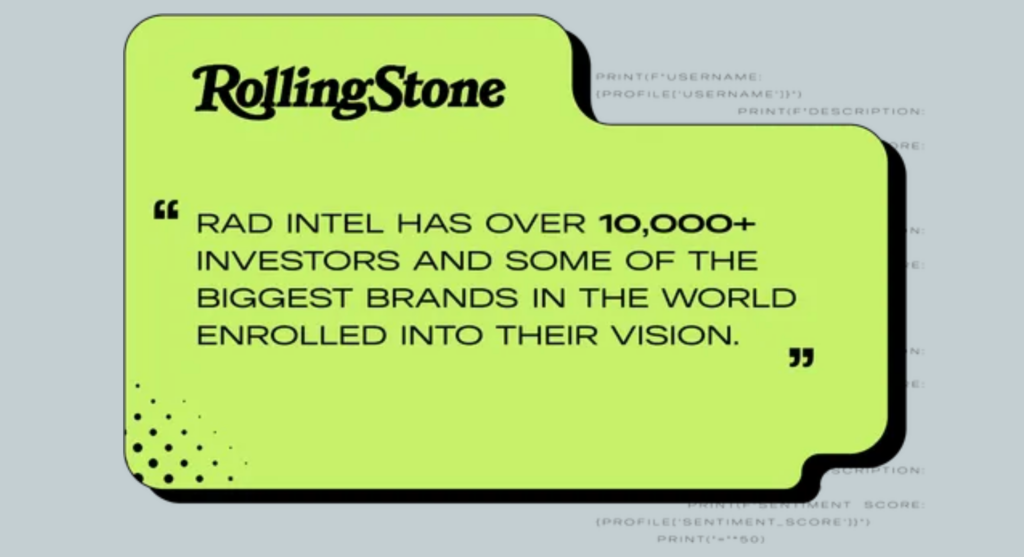

Concern #1

- Claim: RAD Intel’s investor portal included a press quote that it sourced to Rolling Stone. It also used the magazine’s logo next to a broader claim about “buzzing” press coverage.

- Reality: The unlinked excerpt quotes from sponsored editorial content, not actual reporting. Rolling Stone itself has seemingly never written about RAD Intel. A separate glowing snippet from Fast Company was similarly from a paid advertorial.

Editor’s note: Though RAD Intel never replied to Hunterbrook’s request for comment, it subsequently made quiet changes to its current offering website to clarify where it was quoting from advertorials.

Concern #2

- Claim: Multiple crowdfunding ads claimed that RAD Intel was “backed” by both Adobe and Fidelity Ventures.

- Reality: Adobe gave the company an $8,000 grant to fund design work, but is neither an investor nor backer. Fidelity Ventures, a former venture capital firm, also never invested. Rather, two funds managed by Fidelity Investments Canada, which is not a venture capital firm, joined a 2018 bridge round for a Canadian startup that was later folded into RAD Intel.

Editor’s note: The company similarly updated this language after Hunterbrook’s reachout.

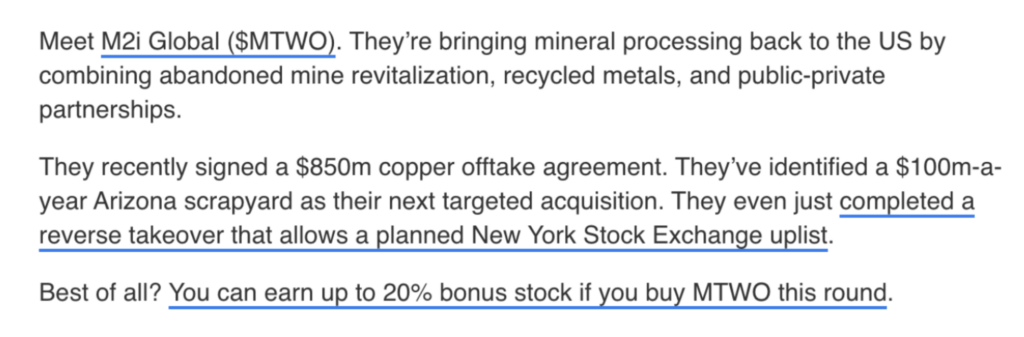

#4 – M2i Global

Stats: 2024 Revenues: $0. Book Value: -$2.5 million. Offered Valuation: $105.1 million. Markup: ∞.

Mineral Metals Initiatives (M2i Global) is more a constellation of ideas than a company. Originally an app development firm, its only reported revenues — around $4,400 total — came from “AI generated tattoo ideas.” It now has vague plans of helping America pull together a critical mineral stockpile.

Though M2i co-released a press release in August 2025 announcing “a transformative public-private initiative to develop and operate the United States’ first Strategic Minerals Reserve,” its CEO clarified a day later, in a YouTube video, that this wasn’t “a done deal.” Months later, it still had yet to sign a storage lease.

M2i ($MTWO), which currently trades as a penny stock, has filed for an NYSE American listing via a reverse merger with an aviation company that, rather poetically, claims to be developing AI for evaluating financial filings. This merger may be complicated by the fact that, in December 2025, M2i lost to a default judgment in a lawsuit it claimed to have not known about. The court awarded the plaintiffs $18 million and 100 million of the company’s shares. That same month, M2i withdrew its Regulation A+ offering after raising $723,000.

Concern #1

- Claim: “Now, backed by federal partnerships and a recent $850m deal, this move sets M2i Global up for national scale.”

- Reality: Hunterbrook found no evidence that M2i has any observable federal partnerships. Additionally, the “$850m deal” was a right for M2i to buy copper offtake up to a fixed amount. It’s also likely moot: M2i’s counterparty, NT Minerals, announced the sale of its interests in the underlying mining area almost seven weeks before this ad went out.

Concern #2

- Claim: “We project our scrap and recycling operation will grow revenue from $3.5M to $8.3M within two years.”

- Reality: While web archives show this claim circulating as early as Jan. 21, 2025, the company’s total 2025 revenues through Nov. 30 were $0. It also continues to own no such operation.

#5 – Pacaso

Stats: 2024 Revenues: $126.5 million. Book Value: $60.3 million. Offered Valuation: $1.5 billion. Markup: 24.9x.

Pacaso sells real estate units that it stresses aren’t timeshares. Its “fractional ownership” solution merely allows buyers to acquire one-eighth shares in vacation homes that Pacaso manages on their behalf.

From a revenue standpoint, this business peaked in 2022. As for profitability, that depends on whether you place weight on Pacaso’s emphasized gross profits (over $120 million to date) or its actual bottom line ($214.8 million in accumulated net losses over the past 4.5 years, with an ongoing cash burn of about $1 million every eight days.)

Over the first six months of 2025, Pacaso spent $9.4 million on ads convincing retail investors to buy in — all while its revenues fell by $23.6 million compared to the same period in 2024.

Concern #1

- Claim: “2024 was a record setting year for Pacaso, reaching a total of over $110M in gross profits and 41% YoY growth.”

- Reality: Beyond the misleading nature of gross profit headlines for a cash-incineration business, this $110 million-plus figure is (non-obviously) cumulative. Pacaso only booked $21.5 million in gross profits in 2024 itself, which was not a record. It also turned this gross profit into a net loss of $31.4 million.

Concern #2

- Claim: “Meet $PCSO. They aren’t publicly traded, but Pacaso just reserved their Nasdaq ticker, $PCSO.”

- Reality: Hunterbrook found that The Wall Street Journal ran this line seven times in its 10-Point newsletter. What’s omitted: Tickers are reserved via a free online form While Pacaso didn’t disclose how it acquired the ticker, the Nasdaq Listing Center only provides one official option. and indicate neither concrete plans to pursue a public listing nor likely success in doing so. Investors were buying illiquid shares in a company with crashing revenues and mountainous losses, not advance tickets for a traditional IPO.

#6 – EnergyX

Stats: 2024 Revenues: $385,000. Book Value: $64.6 million. Offered Valuation: $2.1 billion. Markup: 32.4x.

EnergyX is one of several firms racing to develop direct lithium extraction (DLE) technology to replace traditional brine pool evaporation. The company’s first demonstration plant entered pilot operations in the fourth quarter of 2024. In industry language, a demonstration plan is a successor to a smaller pilot plant. EnergyX’s filings list several pilot plants that never reached that next stage. Though the company’s plant in Chile is the first it has reported having been built to demonstration capacity (50 to 100 tons per year), it has yet to report having produced lithium there at those volumes.

Though EnergyX’s CEO, Teague Egan, claimed in late 2023 that the company would alternate its fundraising between crowdfunders and professionals, it has raised just $262,000 through isolated private sales since, compared to over $100 million from three retail campaigns.

A 2025 DealMaker case study quotes Egan as having spurned venture capitalists who’d argued for lower valuations. This can be read as a self-believing founder fighting for a vision that only he could see. It can also be read as professional money managers being more skeptical of his projections.

Retail investors aren’t experts in industry due diligence. When they read in a Morning Brew ad that EnergyX is a good buy because General Motors alone expects to need “414,469 tons” of lithium carbonate to meet its 2035 EV target, they’re unlikely to realize that this is enough for roughly 7 million EVs. Or that GM — excluding its Chinese joint venture — sold under 4 million total vehicles in 2025, an estimated 5% of which were EVs. They might also not notice that the price of lithium carbonate remains roughly 70% below its 2022 highs.

Concern #1

- Claim: “EnergyX’s patented tech extracts lithium 300% better than conventional methods.”

- Reality: This doesn’t seem mathematically possible. Lithium recovery rates for modern evaporation ponds start at 40% and average about 50%. While yields are lower in unusually magnesium-rich fields in Bolivia, EnergyX’s bid to operate there was rejected in 2022 in favor of competing firms also using DLE technologies. Even if the company extracted at 100% efficiency, doubling the typical 50% baseline would be a maximum improvement of 100%, not 300%.

Concern #2

- Claim: In an October 2025 investor webinar, Egan hyped EnergyX’s steady share price performance: “We went from $8 to $9 and then $9 to $9.50. The shares are at $10 today.” A few minutes later he added that early crowdfunding investors had gotten in at 41 cents per share.

- Reality: There’s a subtle bait-and-switch here. EnergyX “arbitrarily” increased its own valuation in between some of its fundraising rounds, then used share splits to smooth out the impact to its share price. For example, its earliest crowdfunders paid $4.90 per share. Those shares were then split 12-to-1, leaving investors with 12 shares for each one they initially purchased. This is how Egan arrived at a retroactive 41-cent price. But when discussing the more recent increase from $9.50 to $10, Egan left out that those who paid $9.50 ended up with twice as many shares after the March 2025 split. So those paying $10 at the time of the webinar were effectively paying more than double per share, not just 50 cents more. The selective disclosure strategy seems to have worked. Per a DealMaker case study, these webinars raised several million dollars in new investments.

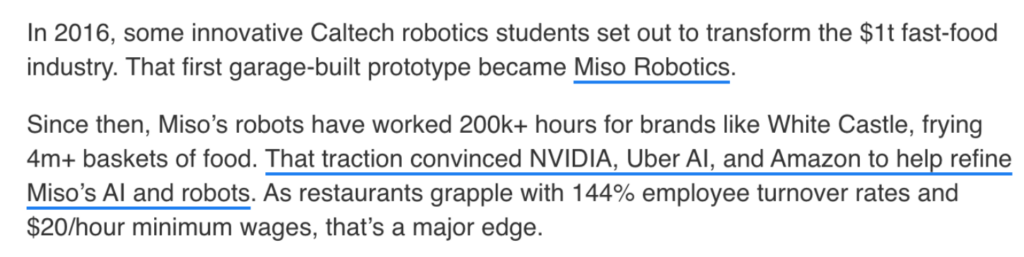

#7 – Miso Robotics

Stats: 2024 Revenues: $384,676. Book Value: $5.5 million. Offered Valuation: $282 million. Hunterbrook didn’t use Kingscrowd’s estimate here as they reflected an outdated share price of $5.22. Shares are now $5.48, multiplied by 51,475,487 pre-financing shares. Markup: 51.6x]

Miso Robotics makes robot arms that fry fast food on behalf of human workers. Its sole marketed product today is the Flippy Fry Station.

“It looks like their main business operation is fundraising and not robot development,” said Tim McLaughlin, a Miso investor. Hunterbrook reviewed an email he sent the company in 2024 to cancel his investment. Miso wasn’t obligated to refund him, and he said the firm never replied. It has gone on to raise over $35 million more since.

Concern #1

- Claim: “Demand for the new third generation of our AI-powered Flippy Fry Station robot is real. Our first production run sold out in a week.”

- Reality: Miso didn’t sell the Flippy Fry Station at the time. It leased the units, with “no upfront costs.” It also had a maximum of three in the field when this sell-out claim first circulated. Online archives show the sell-out claim circulated as early as Oct. 7, 2024. Miso’s initial press release, published Jan. 28, 2025, suggested that pilot units had only been installed at White Castle locations so far, with Jack in the Box and other locations to follow. The company’s next annual report indicated that only four of these units were in the field as of April 9, 2025, with at least one at Jack in the Box. This leaves an upper limit of three units at the time the claim was first made, all at White Castle locations. Over a year later it still had just 14 of these units deployed. It also announced that its pilot with Jack in the Box ended last November with the removal of its final remaining unit.

In a detailed statement, Miso’s CEO, without disputing Hunterbrook’s analysis of the number of units, argued that “sold out” was appropriate given lease commitments for “all available inventory.”

Concern #2

- Claim: In the “2025 onwards” section of its roadmap, as a separate item from its Flippy expansion, Miso’s Innovation Lab was listed as “expanding experimental products for future growth.”

- Reality: While asking investors to credit it for this “future growth” potential, the company simultaneously disclosed in its legal filings that it had discontinued all non-Flippy Fry Station products and R&D for cost discipline.

Miso had previously rolled all “early-stage product development” into its Innovation Lab. When it subsequently shuttered its Cookrite Coffee and Flippy Lite lines, only the Flippy Fry Station project remained.

For emphasis, it added that it would only reconsider if and when “a restaurant partner [commits] to also sharing the development costs of a specific product.”

In his statement, Miso’s CEO outlined incremental technical and support improvements being made to and for the Flippy Fry Station, which Hunterbrook understands to be a single, already-existing product.

The Connecting Thread: DealMaker

In 2018, two corporate fundraising attorneys decided to spin up a new firm, DealMaker, to focus on these new crowdfunding programs. They saw a future in helping startups tell their stories better, especially to retail investors looking for difference-making companies that might notice and value them. As its CEO, Rebecca Kacaba, put it, “People want to make investments in companies that they believe in, that they believe are making a great difference in the world.”

While this is a lovely sentiment, DealMaker makes no bones about who the company actually serves. DealMaker’s customers are the startups, and if those customers want funding then it’s the firm’s job to help. Kacaba was clear on this in a 2024 interview: “We’re not an investor-focused platform.” The firm’s job is to appeal to investors, not to advocate for them.

DealMaker’s strategy worked, with over $2 billion raised for their clients to date across all offering types, including from “hundreds of thousands of individuals and families.” This figure includes some unrelated Regulation D raises.

One key to DealMaker’s success: slick ads. In 2022, it acquired Austin-based agency Ridge Growth, which now operates as its in-house marketing arm. All clients that use DealMaker for their fundraising campaigns have the option of paying extra for help crafting their campaign content — from website copy to email pitches to the sponsored ads supplied to media partners like Morning Brew.

Editor’s note: DealMaker Marketing Services was contracted by all the above issuers, with DealMaker Securities also serving as a broker-dealer.

While DealMaker itself routinely disclaims responsibility for the accuracy of the campaigns it designs, its own client contracts suggest it is deeply involved with the content of the materials:

Again quoting DealMaker’s CEO:

“Our digital marketing team … they do this stuff all the way down to the analytics. They’re monitoring the reactions on the first emails you send, and tweaking the messaging and understanding how to position it to get that deal done.”

But how far did the team tweak? It’s one thing to put your client’s best foot forward, and another entirely to misrepresent key claims to an audience you know is mostly unsophisticated investors.

Especially when you know how ugly the returns are likely to be.

A Legacy of Losses

When the SEC finalized the new rules for these crowdfunding programs in late 2015, DealBook coverage from the New York Times included a dark assessment:

“Ninety-nine percent of these deals will prove to be unprofitable,” said Andrew Stoltmann, a lawyer who specializes in securities fraud. “This is a disaster waiting to happen.”

Young companies need efficient pathways to raise money. There was nothing wrong with giving them more and better options. The foreseeable disaster was adverse selection: Why would a healthy company want the hassles of crowdfunding — e.g., slow financing, bad industry optics, and unwelcome public disclosure requirements — if professional investors were fighting to give them checks? And if the best companies were unlikely to have interest, which companies would?

We saw the same pattern over and over again in our investigation: a company started off with a credible idea, raised money from sophisticated investors, and then failed to deliver results. It was often only then that they found a sudden interest in giving retail investors a seat at the table.

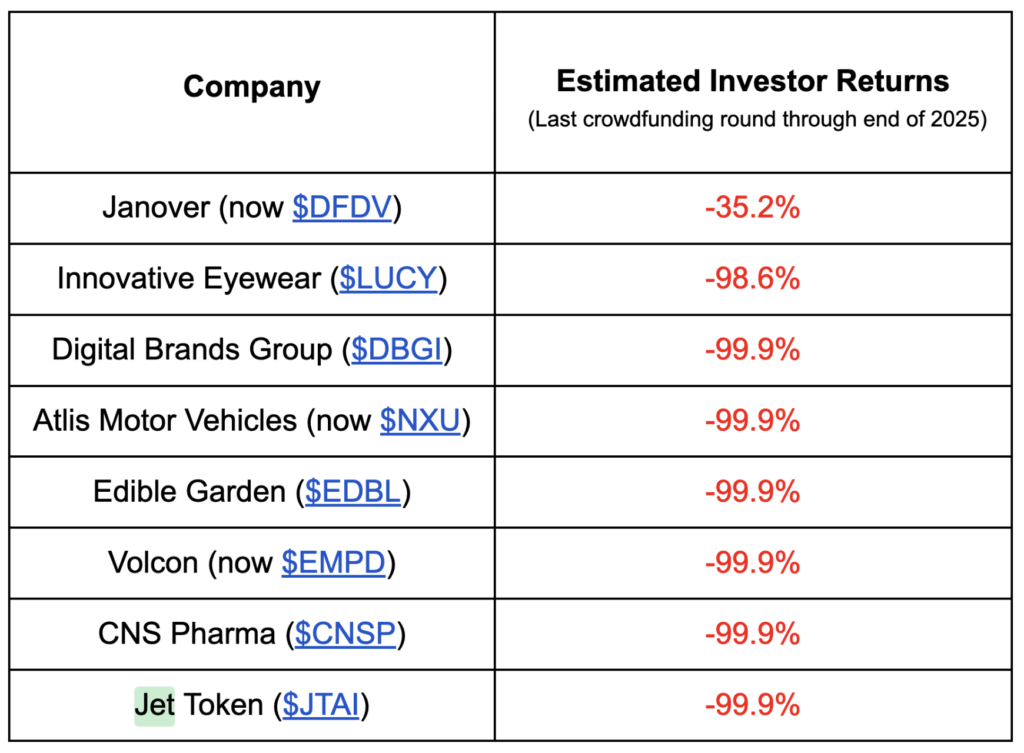

Some of these companies may yet turn the corner and return some money, though history indicates that most will not. Crowdfunding investors can typically only sell their shares when a company goes public or gets acquired, which only 1.2% of all issuers had done as of April 2024.

Even these exceptions are still mostly unhappy stories. To avoid cherrypicking, Hunterbrook analyzed a list from a University of Southern California researcher of Regulation A and CF startups that had filed for a public listing by the end of 2022. Some never crossed the finish line, and those which did all fared poorly. The best of them saw its valuation collapse by 90% before a late crypto pivot partially reversed its fortunes.

DealMaker itself has a similar record. Its two self-touted public listings from 2024 — Sky Quarry ($SKYQ) and Autonomix ($AMIX) — are now down 87.7% and 99.6% respectively from their debut prices. Hunterbrook was only able to identify four other DealMaker issuers that went on to have an exit event. Newsmax ($NMAX) is already trading down 40.5% from its 2025 IPO, Knightscope ($KSCP) and Trust Stamp ($IDAI) are both down over 99%, and Monogram was acquired for a loss of 44.3% along with a promise of uncertain future payments. Monogram used Regulation A+ as its IPO. DealMaker Securities, acting as a member of the selling group, helped it raise nearly $16 million at $7.25 per share. Monogram was then acquired by Zimmer Biomet for $4.04 per share and conditional milestone bonuses. The first of these milestones was paid out in February 2026, which brought net losses from the IPO price down to 29.9%. The next milestone involves a clinical trial currently scheduled for 2027. Despite its name, DealMaker appears to still be chasing a deal that proves successful for its investors.

Of course, staying private doesn’t necessarily mean failure. What about the companies that haven’t gone public or been acquired but really have met their loftiest growth expectations? A recent Morning Brew ad for Pacaso leveraged just such a success story, celebrating a “400x buyout offer” for early crowdfunding investors in the fintech startup Revolut.

While Revolut wasn’t a DealMaker client, there’s a larger issue with this reading: These lucky few investors didn’t actually get to sell all their shares. They were stuck with largely paper gains for years as professional investors and company insiders sold ahead of them. They learned the hard way that most of these deals are like lobster traps: While everyday investors don’t need to wait to get in, they must often wait a long time to get out — if they ever can.

Authors

Jeremy Arnold is the publisher of The Save Journalism Committee, a newsletter focused on journalism reform. He has also worked as a communications consultant for Silicon Valley startups that fundraised on their real merits. He went to school in Canada “and got very good grades.”

Additional research by Daniel Ptashny.

EditorS

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a B.A. in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life. Sam is based in New York.

Jim Impoco is the award-winning former editor-in-chief of Newsweek who returned the publication to print in 2014. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has a master’s in Chinese and Japanese History from the University of California at Berkeley.

Graphic

Dan DeLorenzo is a creative director with 25 years reporting news through visuals. Since first joining a newsroom graphics department in 2001, he has built teams at Bloomberg News, Bridgewater Associates, and the United Nations, and published groundbreaking visual journalism at The Wall Street Journal, Associated Press, The New York Times, and Business Insider. A passion for the craft has landed him at the helm of newsroom teams, on the ground in humanitarian emergencies, and at the epicenter of the world’s largest hedge fund. He runs DGFX Studio, a creative agency serving top organizations in media, finance, and civil society with data visualization, cartography, and strategic visual intelligence. He moonlights as a professional sailor working toward a USCG captain’s license and is a certified Pilates instructor.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided "as is" without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.