Based on Hunterbrook Media’s reporting, Hunterbrook Capital is short $WULF, long $CORZ, and long a basket of comparable securities at the time of publication. Positions may change at any time. See full disclosures below.

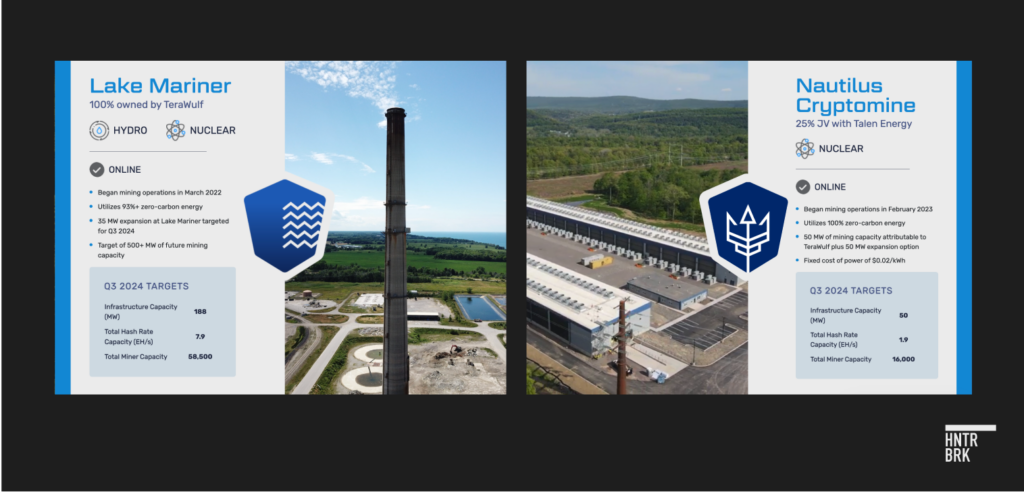

On the shores of Lake Ontario in upstate New York, a dismantled coal plant hums with new energy. Thousands of specialized computers fill cavernous spaces, their fans whirring as they solve complex mathematical problems to mine bitcoin. This facility is Lake Mariner, the key to TeraWulf’s surging operations and its bold promise: zero-carbon bitcoin mining.

Google TeraWulf and you see this:

Click on the link, and you get the same message, against a backdrop slideshow of nature, solar panels, and powerful waterfalls that invoke images of clean hydropower.

Executives tout TeraWulf’s focus on sustainability as a key differentiator across podcasts and YouTube channels. “We wanted TeraWulf to be about zero-carbon,” CEO Paul Prager said in an interview, citing a desire to appeal to “institutional investors.”

The company’s stock price has nearly doubled in the last six months, amid promises of eco-friendly practices and hints of a lucrative pivot to hosting “green” AI data centers. “All these guys want to be able to be out there saying that they are sensitive to ESG guidelines,” CEO Prager told an interviewer, referring to potential customers for TeraWulf’s data centers.

But an investigation by Hunterbrook reveals a gulf between TeraWulf’s public image and its operational reality.

TeraWulf appears to be engaged in widespread greenwashing and misleading advertising about its supposed key differentiator — according to months of research spanning town council meeting notes, electricity contracts, local news reports, and other data available through the New York state open data initiative, as well as interviews and correspondence with energy experts and state regulators.

The company’s keystone Lake Mariner facility, which TeraWulf boasts runs on 93% zero-carbon energy, does not appear to use any energy that can be legally characterized as renewable. “Currently, none of the power that NYPA provides the firm can be claimed as renewable power,” the New York Power Authority, which provides 45% of the facility’s load, told Hunterbrook in an email.

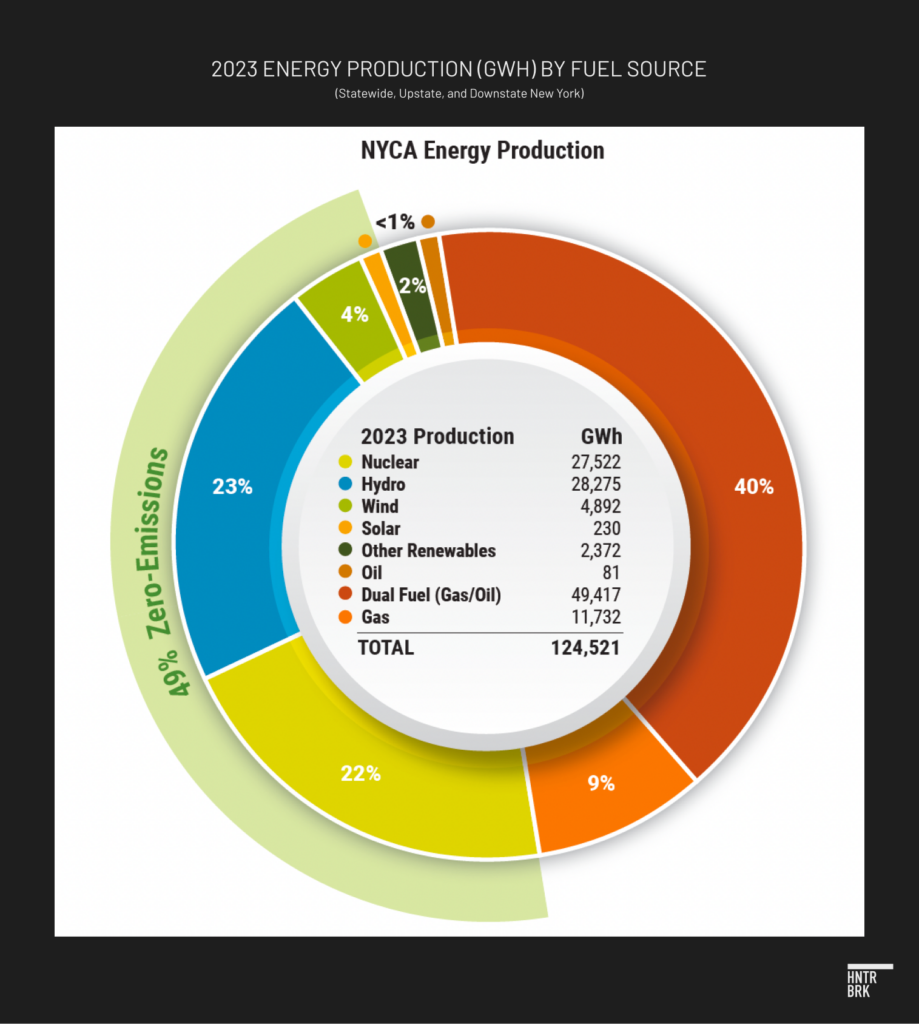

TeraWulf buys the rest of Lake Mariner’s power from New York’s electrical grid, like most other businesses and residents in the state. And New York’s grid is only 49% carbon-free, according to the New York Independent System Operator — powered by a cocktail of nuclear, hydro, wind, oil, gas, and other sources of energy.

TeraWulf executives say the company takes advantage of surplus power in New York and cite the facility’s geographic proximity to renewable energy producers upstate to back up their claims. A spokesperson told Hunterbrook that TeraWulf prioritizes “locations rich in zero-carbon resources” and claimed the facility is located in a zone where ”91% of the electricity generated … comes from zero-emission sources.”

Neither claim makes sense, according to guidelines published by the Environmental Protection Agency, the National Association of Attorneys General, and the National Renewable Energy Laboratory — because there is essentially no way to physically track the electrons from energy producers to consumers on the New York grid.

In other words, TeraWulf’s location near where renewables are produced does not give it the legal right to market that the energy it consumes is renewable — any more than other firms operating in upstate or downstate New York.

In fact, according to Marguerite Wells, executive director of Alliance for Clean Energy New York, “Any crypto facility that is adding its load upstate is automatically doing it with a gas plant.”

“There is no other way,” she told Hunterbrook.

To legally substantiate claims of renewable energy use, New York requires companies to purchase renewable energy credits, or RECs, which represent units of renewable energy produced on the grid. TeraWulf has not purchased any — instead criticizing RECs as not being a true measure of whether or not a company is zero-carbon.

Beyond potential greenwashing, the investigation also shined light on a network of related party transactions and stock sales between TeraWulf and CEO Prager’s companies that may indicate widespread self-dealing.

In one example, TeraWulf paid $20.3 million in management and service fees last year to Beowulf Electricity & Data, which Prager owns and runs as president, for services running the gamut of building and operating bitcoin mines — functions that TeraWulf says are “readily available from independent entities.”

This payment represented 38% of TeraWulf’s operating and administrative expenses and more than half of the company’s operating losses that year.

But Beowulf is just one piece of the puzzle. TeraWulf’s Lake Mariner facility, a cornerstone of its operations, is leased from another entity 99.9% owned by Prager.

Last year, TeraWulf paid this company $887,050 for rent and associated costs. And the prior year, TeraWulf issued that entity 8.5 million shares, valued at $11.5 million.

That was 59 times more than TeraWulf had been expected to pay to Prager’s company in rent over the combined 13-year period of the lease.

Sign Up

Breaking News & Investigations.

Right to Your Inbox.

No Paywalls.

No Ads.

The TeraWulf Story Begins With Coal

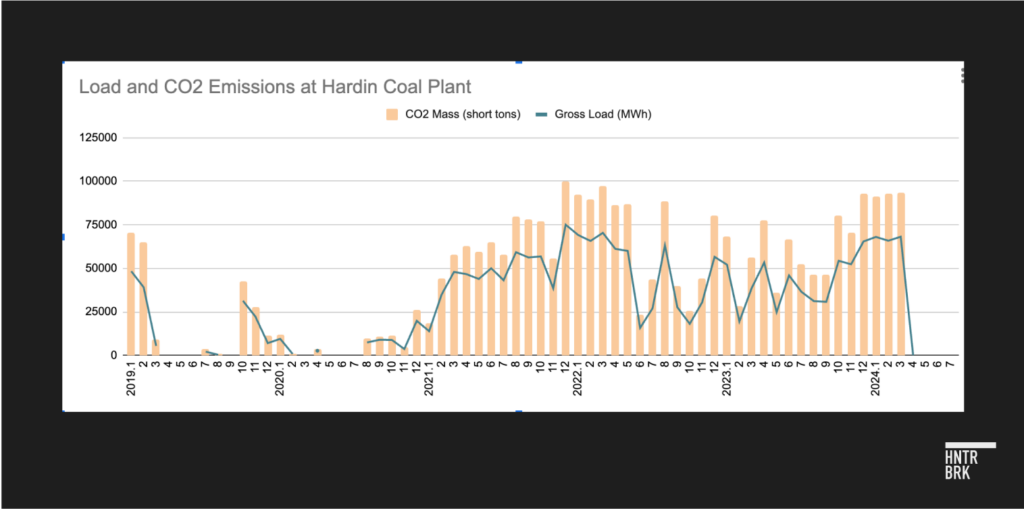

By late 2020, Hardin Generating Station, a coal plant located in Big Horn County, Montana, was on its last legs — operating only 37 days that year. As supplies of cheaper alternatives from natural gas to renewables grew more plentiful, the economics of operating a coal plant had become untenable.

In 2017, Prager’s company, Beowulf Energy LLC — which owns and operates the 115-megawatt plant — told Montana regulators that it expected to close the plant by 2018 due to continuing losses. Local environmental groups waited for the plant to fizzle and shutter.

Then Beowulf found a lifeline. In October 2020, a bitcoin mining company, Marathon Holdings (NASDAQ: $MARA), announced it had signed a contract with Beowulf to build a warehouse stacked full of specialized, electricity-guzzling computers designed to mine cryptocurrency. It became Beowulf’s sole customer.

The contract brought back the dying plant, which had generated a meager 62,000 megawatts in 2020. By the following year, it had produced 566,000 megawatts — a ninefold increase — according to the EPA’s Clean Air Markets Program Data analyzed by Hunterbook. The additional load led to a proportional 900% jump in the plant’s carbon emissions.

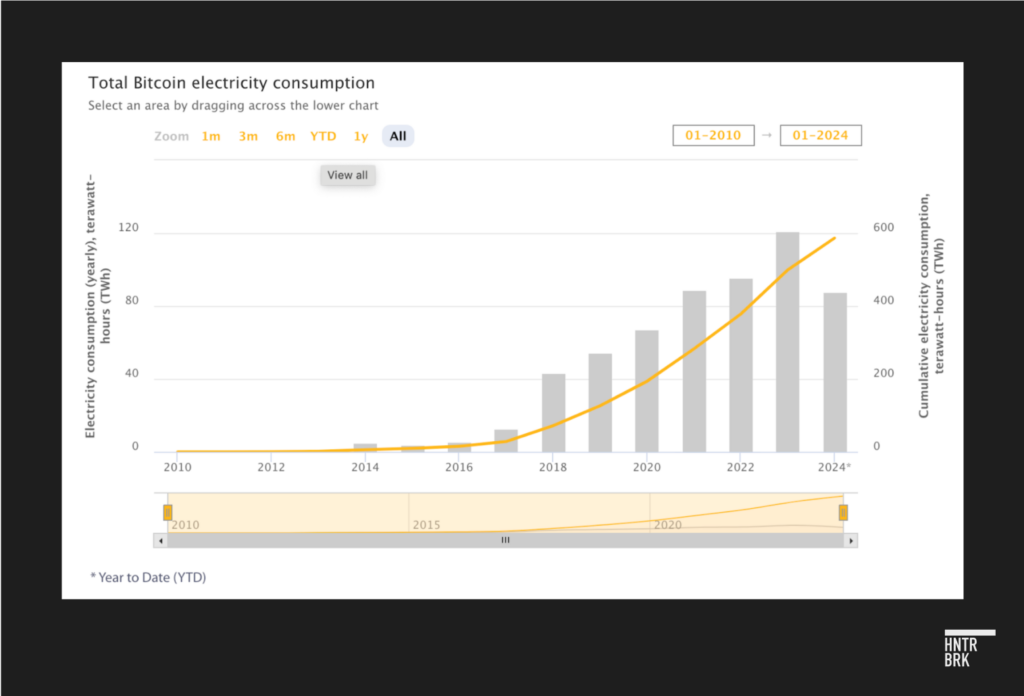

Bitcoin mining’s carbon intensity is the result of a hard-coded feature that makes bitcoin exponentially more difficult to mine over time, as more miners attempt to do so. It was meant to keep the overall supply in circulation limited, with power costs and consumption going up as a side effect.

When the bitcoin protocol was first released in 2009, hobbyists could mine bitcoin on their personal computers. As the value of bitcoin increased, companies began launching industrial-scale mining operations using thousands of specialized machines, known as application-specific integrated circuits, which have exponentially greater computational power than personal computers and consume significantly more electricity.

The resulting bitcoin arms race is a classic prisoner’s dilemma: Each marginal gain attained by mining companies is quickly neutralized as other companies follow suit. That in turn decreases the rewards for all companies, pushing them to deploy even more computing power. The increasing difficulty of mining, combined with the protocol’s built-in halving of mining rewards approximately every four years, ensures the race continues, leading to greater and greater demand on electricity.

According to an estimate by the Cambridge Bitcoin Electricity Consumption Index, the bitcoin mining industry last year consumed about the same amount of electricity as Greece or Australia and is on track to consume more this year.

Just two years into Marathon’s operation at its new mining site in Hardin, it announced it was ending the contract with Beowulf and moving to “new locations with more sustainable and non-carbon emitting sources of power.”

But despite Marathon’s exit, Beowulf’s brief foray into the world of bitcoin mining in Montana did not deter its executives from pivoting into cryptocurrency.

“That’s in 2018-2019, and we really started our journey of saying hey, we should be taking our power and mining bitcoin,” Terawulf co-founder and Chief Operating Officer Nazar Khan said in a recent interview.

Together, Beowulf executives — including Khan, who closed the deal with Marathon — set out to transform the company’s two legacy coal plants in New York, both slated for shutdown as part of the state’s ambitious climate goals, into bitcoin mining facilities.

In 2021, they launched their new company, TeraWulf, with a management team consisting almost entirely of former Beowulf executives, led by Beowulf founder and owner Prager, now also CEO of TeraWulf. TeraWulf executives, including Prager and Khan, likely continue to oversee Hardin’s operations — as their employment contracts with TeraWulf explicitly permit their continued involvement in the coal plant.

TeraWulf Founders Pitched New York Under the Pretense That It Was “Not Targeting Bitcoin or Any Other Cyber Currency” — And Tried to Power Its Operations with Gas

Bitcoin mining companies began flocking to New York in 2018, attracted by upstate New York’s abundance of cheap energy.

But as the state realized the unrelenting appetite of bitcoin miners for the state’s energy resources — often at the expense of local residents — the mood quickly turned. Municipalities began enacting moratoriums and zoning laws to prohibit bitcoin miners from their towns, including Beowulf, the company run by TeraWulf’s founders.

A study by the University of California, Berkeley, later found that cryptocurrency miners in upstate New York had pushed up annual electric bills by about $165 million for small businesses and $79 million for individual households.

Amid the backlash, TeraWulf’s executives initially pitched the idea to state regulators and residents of building an “Empire State Data Hub” at the two coal plant sites.

It would provide computing capacity for “artificial intelligence programming” and “large computational modeling,” like migratory bird mapping and reforestation modeling, the company said in a 2019 memo reportedly sent to the county legislature.

But TeraWulf made itself very clear: “We are not targeting bit coin [sic] or any other cyber currency.”

In the 2019 memo, which was reportedly circulated by Beowulf’s Vice President of Project Management Jerry Goodenough — now also “Upstate Director” at TeraWulf — the company demanded 125 MW of power from NYPA for the data centers.

If denied, the memo said, the company could revert to its old plan to convert one of the coal plants in Lansing, New York, to a gas plant, feeding it with up to 60 truckloads of natural gas a day. As an alternative, the memo said, the company could “sue the State on its proposed coal regulations designed to close only these two plants.”

To boost its credentials, TeraWulf referred to its executives’ success in a similar “coal plant-to-data center project” in Hardin, Montana, not yet online as a crypto mine at the time, according to the local news website Investigative Post.

Despite Beowulf’s efforts, the plant was decommissioned in 2020, earning it the distinction of being the penultimate coal plant to be shut down in the state.

Plans to convert the Lansing plant to a bitcoin mining facility also faltered, after the Lansing Town Council proposed a local zoning law in 2022 to prevent crypto mining facilities from being built in the community. The town council was “blindsided” by the company because it was under the impression the data center would not be used for mining cryptocurrency, according to the Ithaca Times.

But Beowulf eventually found success in turning its other coal plant, in Somerset — the last coal plant to retire in New York — into the bitcoin mining operation that became Lake Mariner, the focal point of TeraWulf’s operations.

TeraWulf’s “Zero-Carbon” Claims Contradicted By State Energy Officials And Experts

Lake Mariner is one of two mining sites that TeraWulf operates — along with the Nautilus Cryptomine in Pennsylvania.

It’s the one TeraWulf claims is powered by 93% zero-carbon energy. But Hunterbrook’s examination of TeraWulf’s disclosures and NYPA meeting notes reveals that none of Lake Mariner’s energy is sourced specifically from hydroelectric power plants or other renewable sources, but rather from New York’s power grid and the wholesale energy market through various providers.

Lake Mariner currently receives 90 MW of its 195 MW capacity from NYPA under the high load factor power (HLF) program, according to TeraWulf’s filings. In a video that TeraWulf posted on X, CFO Patrick Fleury described this arrangement as the company getting “a long-term contract to buy wholesale power from Niagara Falls.”

But in an email to Hunterbrook, NYPA stated that the HLF program “does not have NYPA hydropower tied to it.” Unlike NYPA’s other economic development programs like ReCharge NY — which allocates renewable power sourced directly from hydropower plants in upstate New York to eligible businesses The total 910 MW Recharge NY is a total of 910 MW of electricity that it grants to eligible customers under long-term contracts. It is 50% hydropower and 50% from the market, according to NYPA. — HLF is simply a “market based program” that sells power that NYPA purchases from the wholesale energy market.

The rest of Lake Mariner’s energy comes from the grid, which derives 49% of its energy from clean sources, according to the annual Power Trends report published by the New York Independent System Operator Inc.

This is the same source that TeraWulf has used — both in security filings and in its response to Hunterbrook’s request for comment — to support its zero-carbon claim. But the report clearly says 91% of energy produced — not consumed — in upstate New York is green.

The company also points out that Lake Mariner is merely 40 miles from one of the state’s largest hydroelectric power plants, the Niagara Power Project.

But that is not how the grid works.

Being physically close to a renewable energy source is not a legal — or scientific — basis for renewable energy claims, according to Hunterbrook’s review of federal and state guidelines on green claims.

“Due to the physical nature of electricity and the way it moves across the shared electric grid, it is difficult for consumers (or utilities) to know precisely the source or origin of the electricity they consume, even with onsite projects,” the EPA wrote in public guidance.

To address this problem, New York, like many other states, uses a system of RECs, which represent units of renewable power, to track the economic value of renewable energy moving through the grid. It grants purchasers of the RECs the legal right to claim that the energy it sources from the grid is renewable. This is designed to be in line with the FTC’s Green Guides, which disallow marketers from making unqualified renewable energy claims unless they purchase RECs.

“Without the REC, there is no legal claim to the renewable attributes of electricity,” a spokesperson for the New York State Energy Research and Development Authority — a state agency mandated by the State to manage the REC system — confirmed in an email to Hunterbrook. The spokesperson called RECs “the legal instrument that certifies ownership of the environmental attributes of electricity in New York.”

The FTC is currently taking steps to update the Green Guides for the first time in 11 years. “Corporate sustainability claims are expected to come under fresh scrutiny,” reported the Financial Times. The FTC’s review coincides with the Security and Exchange Commission’s recent moves to strengthen oversight over climate-related disclosures, including by enacting a new rule in April requiring most public companies to make extensive disclosures about climate change.

And RECs aren’t cheap.

In 2023, one renewable energy certificate, representing one megawatt hour, issued by NYSERDA cost at least $7.95. To avoid violating New York’s rules, which are adaptations of federal guidelines on deceptive green marketing, the 195 MW Lake Mariner facility running at full capacity would have to buy roughly $13.5 million in RECs a year to substantiate its zero-carbon claims. That is nearly half of what the company paid for electricity last year.

At a full 500 MW capacity, as TeraWulf says it plans to scale to, the total cost would be about $34.8 million a year. This would increase TeraWulf’s annual cost of revenue by 60%. It would also bump up the company’s cost of energy close to the industry average of five cents per kilowatt hour, undermining TeraWulf’s low-cost energy claims. REC purchases would bring the average cost to roughly $0.048/kWh, according to Hunterbrook calculations based on the price of Tier 2 RECs sold by NYSERDA of $7.95 per megawatt hour, the average energy cost so far this year of about $0.040/kWh, according to the company’s monthly disclosures, and the annualized Q1 2024 cost of revenue of $14.4 million.

TeraWulf also says it uses surplus power that, in the words of CFO Fleury, “otherwise would effectively go to waste.” CEO Prager adds that TeraWulf’s competitiveness comes from having “scalable sites where there is excess supply of energy.” But as reported by New York Focus, NYPA, which produces most of New York’s hydropower, denied creating a surplus. The power it generates “gets sold, whether to the public sector or to the wider market.”

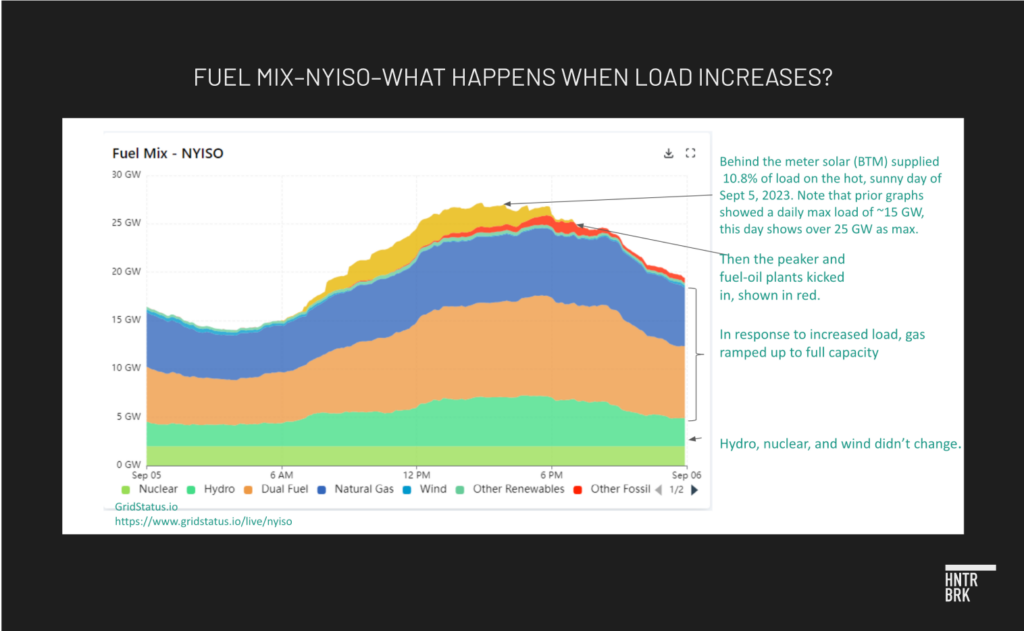

Wells confirmed that there is no excess renewable energy in New York, citing her extensive research on the New York electric grid. She explained that hydroelectric and nuclear plants in New York were always running at maximum capacity, even before bitcoin miners came to the state. “Gas plants are actually running all the time at like half output,” she said.

When demand “ramps up,” she explained, “the gas plants double their output.”

Furthermore, New York has four peaker gas plants — plants that kick into gear during peak demand — that it plans to keep operating past their expected 2025 retirement age to meet an expected deficit of 446 MW amid rising demand, according to the NYISO.

“We had been moving away from relying on peaker plants to take care of excess energy needs, but after crypto started expanding, the NY grid was purchasing more and more power from natural gas peaker plants,” Colin Read — professor of economics and finance at State University of New York Plattsburgh and author of The Bitcoin Dilemma — told Hunterbrook via email.

“If this additional dirty power is fed into the grid primarily because of enhanced demand from crypto,” he said, “then in fact their power demand is anything but green.”

TeraWulf does have a legitimate claim to green energy through its 25% stake in the Nautilus Cryptomine, a 200 MW facility it co-owns with Talen Energy (NASDAQ: $TLN), which provides energy from its nuclear power plant.

But Talen is looking to sell its majority share of Nautilus, according to a Reuters report on August 1, citing three sources familiar with the process: “If Amazon Web Service buys out its tenants, the giant tech company could swiftly access the 200 MW of electricity instead of waiting years, the sources said.”

Talen already sold the campus on which Nautilus is located to AWS for $650 million earlier this year — and the company’s filings state that it can terminate TeraWulf’s lease at any time, unilaterally, without TeraWulf’s consent. Talen has already transferred the lease to an AWS affiliate.

CEO Paul Prager at Center of Related Party Transactions and Stock Awards

Greenwashing may not be TeraWulf’s only potential sleight of hand.

An examination of TeraWulf’s corporate structure reveals extensive related party transactions and stock disbursements from insiders. Hunterbrook’s analysis is based on the company’s SEC filings, including registration, proxy, and annual statements, available on EDGAR.

At the heart of this web is Prager.

Prager has been known to split his time between a “five-bedroom Fifth Avenue co-op” in Manhattan and a sprawling 250-acre estate on Maryland’s Eastern Shore, according to a 2021 profile in Washingtonian. This estate, called Maiden Point Farm, is described as “more like a small village with 20 structures,” including a “main house, English-style gardens, a pool, a tennis pavilion, a squash court,” and even a private gas station for his car collection, which includes multiple Ferraris.

Hunterbrook’s analysis of the company’s SEC filings shows TeraWulf’s operations are deeply entwined with a constellation of entities under Prager’s control, making it difficult to discern where TeraWulf ends and Prager’s other interests begin.

Beowulf Electricity & Data, While Beowulf Electricity & Data Inc. appears to be distinct from Beowulf Energy LLC, Beowulf Energy & Data’s website states the company is an “evolution” of Beowulf Energy LLC, and lists the assets previously owned by Beowulf Energy. The company in 2021 initially refused to answer the SEC’s request for more information on Beowulf E&D’s history, saying that Beowulf E&D commenced operations in 2021 and therefore has no operating history to report. The company later provided a limited set of financials for Beowulf E&D, which revealed that the entity had minor resources ($1.1 million of total assets) and minimal business activity ($1.9 million of sales, presumably all from TeraWulf). There is no recent public information on Beowulf Energy. a company owned and controlled by Prager, provides TeraWulf with “infrastructure, construction, operations and maintenance and administrative services necessary to build out and operate certain Bitcoin mining centers” — functions that TeraWulf claims are “readily available from independent entities.”

In 2023, TeraWulf paid $20.3 million to Beowulf for these services, representing 38% of TeraWulf’s combined operating and administrative expenses. It also accounted for more than half of the company’s $29.4 million operating loss for the year. The trend continued into 2024, with TeraWulf recognizing $3.5 million in related party expenses in the first quarter alone, amounting to 21% of its operating and administrative expenses for the quarter.

Compare this to a similar deal Beowulf had with the Nautilus Cryptomine — which Prager does not control. Under that arrangement, Beowulf received just $750,000 annually for doing similar work. When the deal was cut short, Beowulf received a $1.75 million termination fee.

Adding another layer of entanglement, TeraWulf has engaged in multiple private placements with Allin WULF LLC and Lake Harriet Holdings LLC — entities controlled by Prager and Khan, respectively.

By participating in these placements, Prager and Khan potentially gain access to company shares at preferential prices not available to the general public or other shareholders. This could create a conflict of interest, since the executives were effectively on both sides of the transaction.

Placements like this often result in the issuance of new shares, diluting the ownership stake of existing shareholders who are not part of the deal.

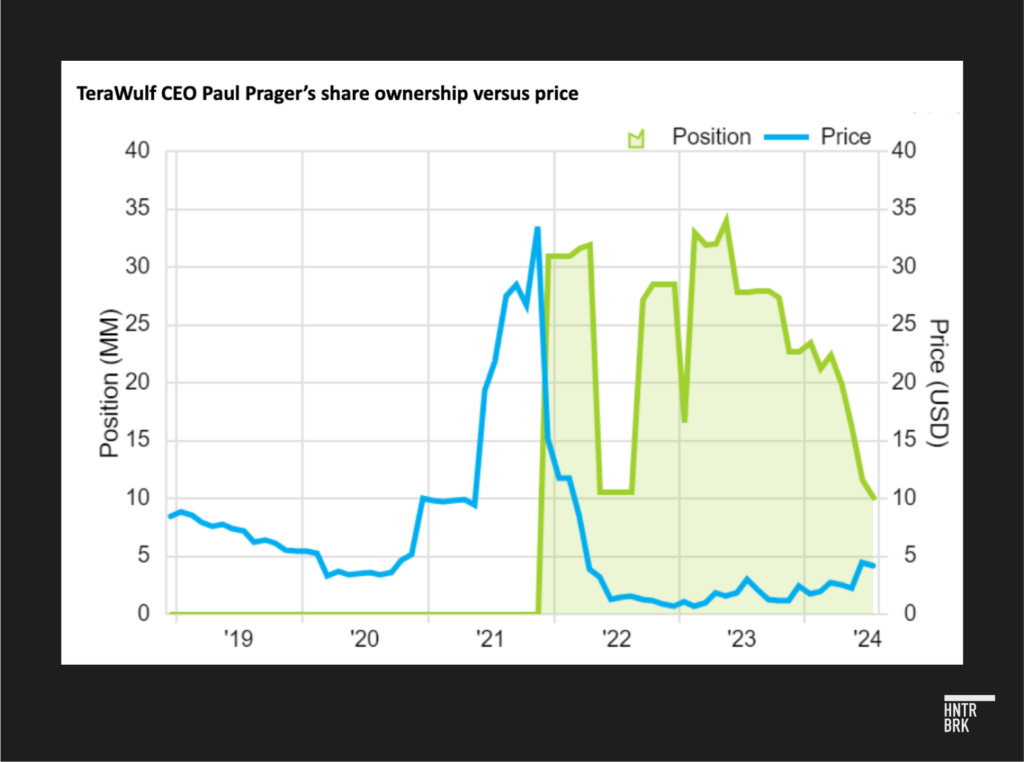

In recent years, Prager has received a significant quantity of TeraWulf shares — through both the related party transactions and financial activities. And in an open letter published early in 2023, he shared that he hadn’t “sold a share” as “evidence of my conviction.” But since mid-2023, Prager has significantly reduced his claimed ownership of the company through a series of stock disposals.

His reported ownership has dwindled, with his holdings falling to around 10 million shares compared to more than 30 million shares in 2023.

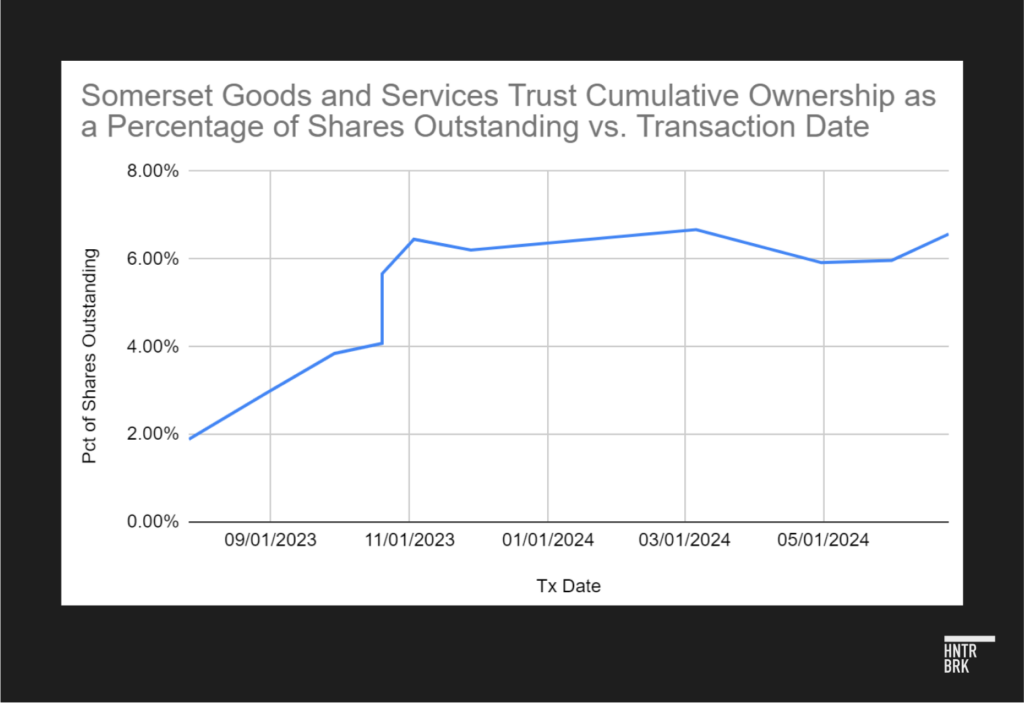

But a mysterious entity, called “Somerset Goods and Services Trust,” complicates the story. Since mid-2023, this shadowy trust has silently amassed a fortune in TeraWulf shares contributed by executives Prager and Khan. At current market rates, this adds up to about $80 million.

Prager and Khan have contributed approximately 21.4 million and 0.5 million shares, respectively, to this trust “for no consideration,” according to SEC data. Unlike other companies controlled by these executives, the ownership and control of Somerset Goods and Services Trust remains unknown.

The trust’s holdings, if left untouched, would constitute 6.57% of TeraWulf’s outstanding shares — enough to trigger mandatory SEC disclosures. Yet, public records remain conspicuously nonexistent. This glaring absence suggests two potential scenarios: either Somerset has flouted federal reporting laws, or it’s strategically offloading shares to sidestep regulatory scrutiny by staying below the 5% threshold.

In response to a question about the entity, TeraWulf stated: “The Somerset Goods and Services Trust is not controlled by Mr. Prager or Mr. Khan and has no financial relationship with TeraWulf.”

Asked a follow-up question regarding whether either executive held a financial interest in the entity, directly or indirectly, TeraWulf demurred — simply repeating a version of its prior answer.

The Somerset name, however, has followed Prager throughout his career.

In 1979, he incorporated a company called the Somerset Railroad Corporation. And in 2012, he founded the Somerset Operating Company, which owned a coal plant in upstate New York.

That plant would eventually mine bitcoin and change its name to Lake Mariner.

Appendix: AI Data Center Payouts Could Be “7+” Years Out

TeraWulf is among a handful of bitcoin mining companies whose stock prices recently rose steeply after their pivot to hosting high-performance computing (HPC) data centers, often used for AI-related tasks. Bitcoin miners share some basic infrastructure requisites with HPC data centers, including stable, long-term, low-cost power contracts. A recent $4.7 billion hosting deal by bitcoin miner Core Scientific (NASDAQ: $CORZ) with AI company CoreWeave added to the excitement, with investors expecting other bitcoin miners to soon follow suit.

TeraWulf has not resisted the hype, with the management team suggesting it could land a similar deal. CFO Fleury specified in an earnings call earlier this year that, by leasing out all of the 300 available megawatts at Lake Mariner, the company could bring in $300 million to $450 million in hosting revenues a year. TeraWulf’s revenue last year was $69 million.

TeraWulf doesn’t yet have AI-ready facilities, unlike competitors who made the switch to HPC data center hosting years ago. But TeraWulf announced it is on track to build a 2 MW experimental AI data center by the third quarter of this year and plans to build another 20 MW data center with a target completion date of the end of 2024.

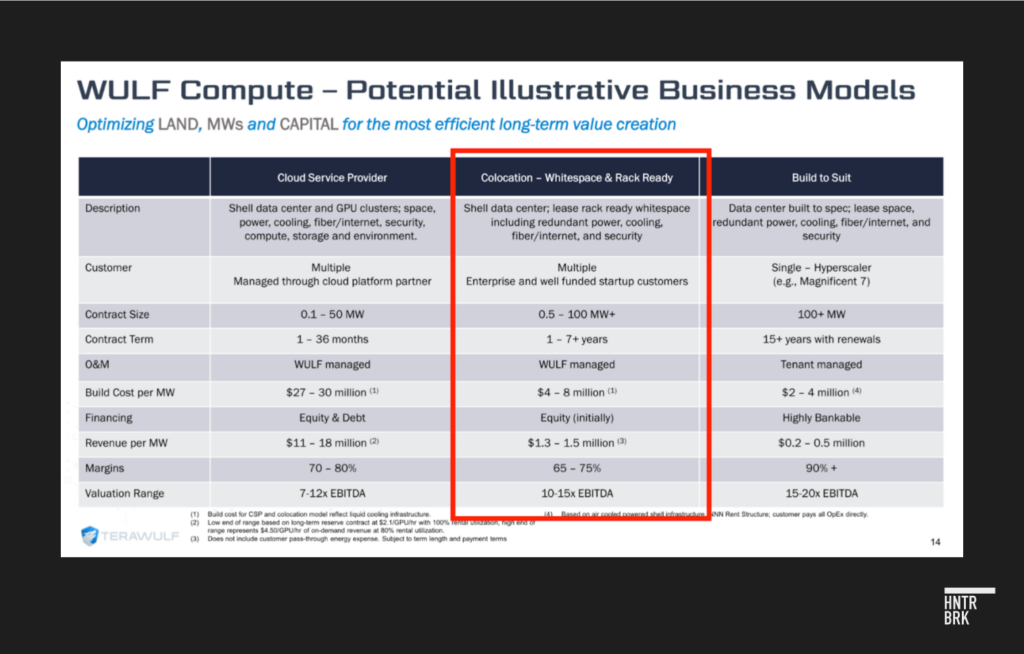

TeraWulf’s new business model is to provide colocation services — in other words, leasing out empty data centers — to an aggregate of AI companies with their own GPUs. This strategy could take 7+ years to recoup the costs, according to a company executive.

And in a statement to Hunterbrook, TeraWulf said: “The Lake Mariner site is equipped with the fundamental requirements for high-compute data centers, including redundant core electrical infrastructure, ample access to water for advance liquid cooling, and a dual-path high-speed fiber infrastructure.”

Two other models the company weighed had a payback period of three years or less with larger margins, but company executives said they are not currently focusing on those and might pursue them if there were a financial opportunity.

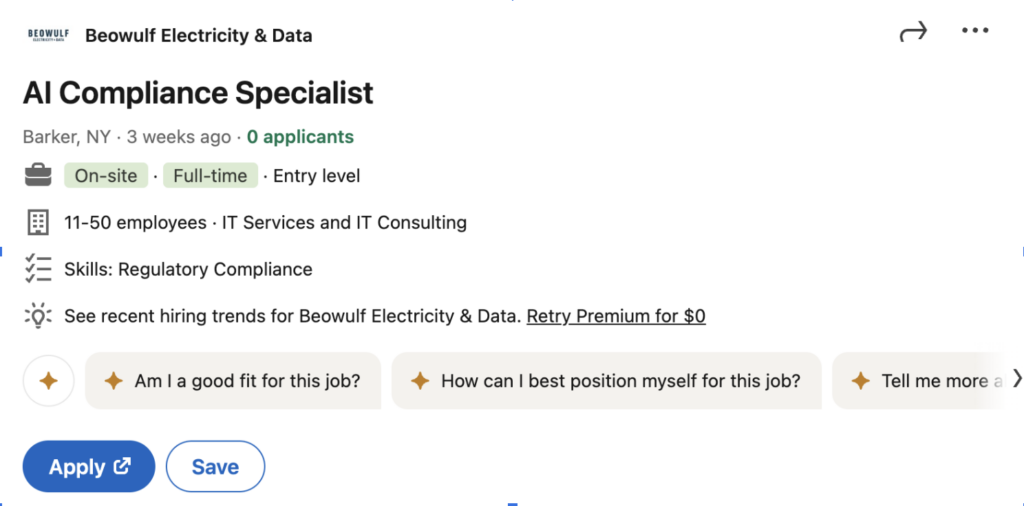

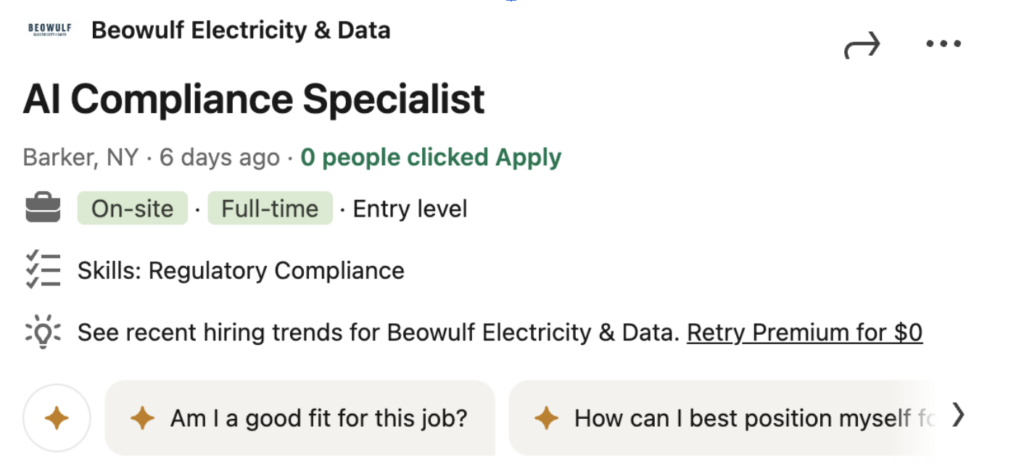

Then there is the apparent mismatch with the local talent pool. A TeraWulf recruitment ad on LinkedIn for an AI compliance specialist at the Lake Mariner site — posted recently on two separate occasions — still has no applicants.

Authors

Jenny Ahn joined Hunterbrook after serving many years as a senior analyst in the US government. She is a seasoned geopolitical expert with a particular focus on the Asia-Pacific and has diverse overseas experience. She has an M.A. in International Affairs from Yale and a B.S. in International Relations from Stanford. Jenny is based in Virginia.

Nick Gibbons, who also contributed reporting, is a seasoned forensic accounting expert and investment researcher. His experience includes a blend of qualitative and quantitative investment roles at Two Sigma, Norges Bank Investment Management, and Citadel. He began his career in forensic accounting at independent equities research provider Gradient Analytics. He additionally has a background in graduate level education having previously served as Adjunct Professor of Finance and Accounting at Thunderbird School of Global Management and currently as Adjunct Assistant Professor of Accounting at NYU Stern School of Business. He is a Certified Fraud Examiner (CFE) and Master Analyst in Financial Forensics (MAFF).

Editors

Jim Impoco, the editor-at-large at Hunterbrook Media, is the award-winning former editor-in-chief of Newsweek. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has an M.A. in Chinese and Japanese History from the University of California at Berkeley.

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets. He has a B.A. in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided "as is" without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.