Based on Hunterbrook Media’s reporting, Hunterbrook Capital is long $SDGR at the time of publication. Positions may change at any time. See full disclosures below.

Schrödinger (NASDAQ: $SDGR) uses quantum mechanics to design new medicines and materials. All top 20 pharmaceutical companies buy its software. Schrodinger’s SEC filings and website claim that the top 20 pharmaceutical companies by revenue are all customers. Many startups pay it royalties and equity in deals worth tens of millions to access its platform. The Eli Lilly acquisition of Morphic Therapeutics Inc. resulted in $47.6 million to Schrödinger. The Takeda Pharmaceutical Co. Ltd. acquisition of a Nimbus Therapeutics subsidiary resulted in $111 million to Schrödinger.

Schrödinger is also a key AI winner. It benefits from falling GPU chip costs, a Nobel-winning prediction model from Google DeepMind that opens up new targets for drug discovery clients, and the enhancement of the company’s physics engine with machine learning.

So why, five years since its IPO, was Schrödinger trading around its all-time low?

Interviews with industry experts, investors, former employees, and Schrödinger’s CEO — alongside a review of its products, financials, SEC filings, and AI papers — reveal a company whose part-biotech, part-software business model has proven hard to value.

Now Schrödinger has cautiously embraced AI, announced a new round of deals with partners ranging from Novartis to Nvidia, and this year will report clinical data from its first three internal drugs. As Hunterbrook prepared to publish this article, $SDGR leapt over 30% across two days.

Is it a turning point?

Nvidia CEO Jensen Huang had a message to deliver.

He was hosting Schrödinger CEO Ramy Farid for dinner at Huang’s home in the Bay Area. Nvidia’s chips power the AI boom, and Huang wanted its longtime partner Schrödinger to find more ways to use them. Farid was skeptical.

“There was shouting,” an investor who heard about the meeting from Nvidia’s healthcare team told Hunterbrook, “about a fundamental disagreement on the role of AI in drug discovery and chemistry.”

Farid told Hunterbrook in an interview that his view has since evolved.

Huang had pushed Schrödinger “to think bigger about what’s possible.” At the time, “it didn’t resonate,” recalled Farid, who doesn’t like to “overreact to hype” and found the excessive claims of companies applying AI to biotech “frustrating.”

“Pharma companies have been burned by a lot of over-promise and under-deliver,” agreed Jen Asher, in an interview with Hunterbrook. Asher is the founder and CEO of 1910 Genetics, a Microsoft-backed AI biotech company seeded by OpenAI founder Sam Altman that aspires to solve problems that impeded earlier efforts in computational drug discovery.

Altman and his counterpart Dario Amodei at OpenAI competitor Anthropic have each written that they believe biotech is one of the most promising applications for AI. Schrödinger is perhaps among the best positioned to realize this potential.

“There was a window there where I wouldn’t use the words ML and AI because I was so annoyed,” Farid said. “But on reflection,” he said, it became clear after his conversation with Huang that integrating AI with Schrödinger’s drug discovery tools would be “incredibly powerful.”

“You can imagine this light turning on,” Farid said. “Now we get it.”

He highlighted Schrödinger’s troves of physics data available to train machine learning. “I think there’s no question that we will be able to capitalize on it better than anybody else,” he said.

In July, Schrödinger announced an initiative funded by the Gates Foundation that uses Nvidia’s chips to predict the safety of new medicines — before the medical compounds have even been synthesized in a lab.

“With its world-leading physics-based platform, Schrödinger has spearheaded the last two decades of computational drug and materials discovery,” Kimberly Powell, Nvidia vice president of healthcare, said in a press release.

“Accelerated computing — which introduces many orders of magnitude in discovery power — combined with generative AI will enhance researchers’ abilities to tackle complex scientific challenges like predictive toxicology, leading to faster, more efficient and effective discovery cycles and transformative medicines for patients.”

Yet despite Schrödinger’s unique positioning, its share price recently traded near all-time lows.

One reason may be Farid’s longtime reluctance to get caught up in the AI hype cycle. Or maybe investors struggle to wrap their heads around the rarefied nature of what Schrödinger does, including how to value a company that’s partly a software business and partly a biotech pipeline.

“It is puzzling, given the continued outstanding growth of the software business, the progress on the pipeline, and the billions of value Schrödinger has generated from the NewCos,” Cony D’Cruz — CEO of Nvidia-backed, AI-driven drug discovery company Superluminal Medicines Disclosure: The author is a co-founder of Superluminal and served on the board of directors, but no longer has any financial interest in the company and has not been involved since the spring of 2023. and former chief business officer of Schrödinger — told Hunterbrook in an interview when Schrödinger’s stock price hit a nadir. (NewCos refers to new companies, such as those created with the Schrödinger platform.)

“I can only assume that the public markets find it challenging to absorb complex stories,” D’Cruz concluded.

“They’re really unique in the market,” said Nemo Despot, an analyst at ARK Investment Management, one of Schrödinger’s largest shareholders. “That’s why we have them,” he told Hunterbrook.

“They’re doing too many different things on the strategy side,” he said. “I think it’s confusing. Oh, they’re spinning out companies. They have the software business. There’s a data science business, and then they are developing their own drugs, as well.”

Is Schrödinger software or biotech? It depends who’s looking.

I first met Farid during Schrödinger’s IPO roadshow at the end of 2019 when he pitched the healthcare investment firm where I was working as an associate.

“Our mission is to improve human health and quality of life by transforming the way therapeutics and materials are discovered,” Schrödinger presented in its S-1 filing, claiming that its “software solutions enable the discovery of novel molecules for drug development and materials applications more rapidly, at lower cost, and with, we believe, a higher likelihood of success compared to traditional methods.”

The story divided investors, sell-side analysts, and industry journalists. Would Schrödinger be valued as a software company driven by revenue, a biotech company based on experimental medicines, or a Frankenstein’s monster sum-of-parts?

From quantum chemistry to machine-learned force fields

Two theoretical chemists founded Schrödinger in 1990. Richard Friesner and William Andrew Goddard III. They applied the eponymous wave function to predict what happens to atoms in various settings using quantum mechanics.

“They called it Jaguar because it was fast QM code,” said Woody Sherman, chief innovation officer at Psivant Therapeutics and former global head of application sciences at Schrödinger, using QM to refer to quantum mechanics.

The software can now simulate the strength of a drug candidate or the brightness of an OLED display. This enables users to predict how products will perform, before spending the time and money to actually make them. Then the user can iterate on prototypes within the computer.

The process uses computational tools to make decisions, Sherman explained. “Should you go left, should you go right, should you make this molecule, should you make that molecule?”

He described how tools like Jaguar enabled Schrödinger to grow into an industry leader.

“You started to have folks seeing the progress, people like Bill Gates, who asked: how do we get computers to improve human health?”

David Shaw, the billionaire scientist and investor, funded Schrödinger. He gave it access to his hedge fund’s supercomputer. He also brought the startup over from New Jersey to the floor below his Times Square office, so his engineers could share a staircase with Schrödinger’s.

“By the time I was there,” said Sherman, there was “some competition and things that weren’t flowing very well. The Shaw guys moved to a different tower and that was that.”

Farid began at Schrödinger in 2002 — when he said that the company had just 30 people — after working as an assistant professor of chemistry at Rutgers University.

Fifteen years later, he became CEO.

Schrödinger’s three-headed beast

Today, Schrödinger has three businesses, all related to its mission of improving drug discovery and development. It licenses software-as-a-service. It partners with companies in return for equity, milestone fees, and royalties on drugs developed as a result of the partnership. And it develops its own medicines.

In the first nine months of 2024, Schrödinger made over $100 million in revenue from software and product services, and $18.5 million from drug discovery partnerships. These numbers do not include $150 million up front from Novartis in a partnership deal that closed in November 2024, and could be worth up to $2.3 billion. Nor does it include $47.6 million from the sale of Schrödinger’s stake in Morphic Therapeutic to Eli Lilly in August 2024 “MORF has a Schrödinger-enabled platform teeming with potential,” wrote a pair of BTIG analysts at the time of the acquisition. Schrödinger maintained its royalty on one of Morphic’s products, upside that Jefferies estimated is worth $120 million for Schrödinger at the program’s current stage of development. and its expanded partnership with Otsuka, announced in January 2025.

Schrödinger owns similar stakes in over a half-dozen companies, including around $50 million of Structure Therapeutics (NASDAQ: $GPCR). Schrödinger is estimated to own about 2.9% of Structure Therapeutics, which had a market cap of ~$1.7 billion as of January 2025. Structure is developing a GLP-1 drug to treat obesity. Unlike the GLP-1 injections that made Novo Nordisk and Eli Lilly the two largest pharmaceutical companies in the world by market cap, the Schrödinger-enabled drug is a more convenient pill.

Schrödinger launched these types of equity and milestone payment deals so that smaller companies could afford its platform.

Having co-founded Nimbus Therapeutics in exchange for stakes in its products, Schrödinger received payouts when pharmaceutical companies acquired some of those assets, including $111 million when Takeda bought an experimental autoimmune treatment. Schrödinger helped Agios Pharmaceuticals Inc. (NASDAQ: $AGIO) develop FDA-approved medicines enabled by computational design. It also launched a materials science unit with partners ranging from L’Oreal to Ansys.

In addition to its software sales and drug development partnerships, Schrödinger has been developing several experimental medicines of its own. Three candidates are now in clinical trials, with the first results from each expected in 2025. “We await a flurry of clinical readouts,” wrote Goldman Sachs in a January research note.

“Schrödinger has built a powerful technology platform over 30+ years,” said D’Cruz. “The platform delivers value, as is evidenced by the growth of software revenue, pharma partnerships, clinical progress, and the value it has generated through spinning out companies.”

A partner at a foundation that supports Schrödinger told Hunterbrook: “We see the tools that they’ve been able to develop as fundamentally providing, I wouldn’t describe it as a public good, but a way to increase the productivity of the industry overall.”

Despot agreed. “My thesis, this is an unmet need, they are the only ones doing it at the moment, and so, I think it’s important for us to be there,” he said.

Among those tools: WaterMap for analyzing the thermodynamics of the water molecules that a drug displaces when binding a disease protein. FEP+ (Free Energy Perturbation) for predicting how tightly the drug binds its target. Maestro as a graphical user interface for modeling and collaboration.

“A wild ride” in the public markets

At the IPO, how would the market value such a multifarious business model?

Bullishly, it turned out.

Schrödinger priced its IPO at $17 per share. The stock quickly leapt to $24, raising over $232 million (more than twice the company’s target) in one of the buzziest biotech IPOs of 2020.

A year later — as the sector boomed at the intersection of the pandemic, low interest rates, and massive stimulus — Schrödinger traded up to $110, valuing the company at over $7.5 billion.

Then Shaw and Gates sold a chunk of stock. The biotech bubble popped, kneecapping R&D budgets at many of Schrödinger’s clients and partners. The Inflation Reduction Act became law, including drug pricing provisions that disincentivized funding the type of small molecules that Schrödinger designs, relative to other types of drugs like biologics or cell and gene therapies.

All of this contributed to Schrödinger’s stock falling to $17 by October 2024.

“It’s been a wild ride, right?” remarked Farid.

On November 12, 2024, Schrödinger announced its third-quarter earnings and a major deal with Novartis. The stock initially leaped over 15% but ended the week below where it had begun. In mid-January, the stock was at $19 with a market cap of around $1.4 billion.

Sherman said that investors were asking a simple and not entirely unfair question: “If these tools are so predictive and so wonderful, why aren’t they making more software revenues?”

Schrödinger largely fulfilled the claims made in its IPO roadshow five years ago. Revenue has grown significantly. The company’s software and product services have maintained a 73%-82% margin, despite high spending on growth. Drug discovery has a far more variable margin, with lumpy nature of drug discovery collaborations and payouts. The company has had misses and downgraded guidance, but has also continued to scale up without relying on debt or equity financing.

The internal pipeline led by former Merck executive Karen Akinsanya has also progressed since the roadshow — from the test tube to human studies. Now Schrödinger has to prove it can not only take these drugs from ideation to the clinic, but achieve good data and partner them out.

“Back to the point of Schrödinger’s valuation, I think that one of the big things people are trying to figure out is, ‘Can these people make drugs?’” asked Sherman. “They’re working on targets that are interesting but not novel.”

Farid framed that lack of novelty as an advantage, because it mitigates the biology risk of drug development, putting the focus on the better chemistry Schrödinger has proven it can produce.

“We’re working on validated targets,” he told Hunterbrook.

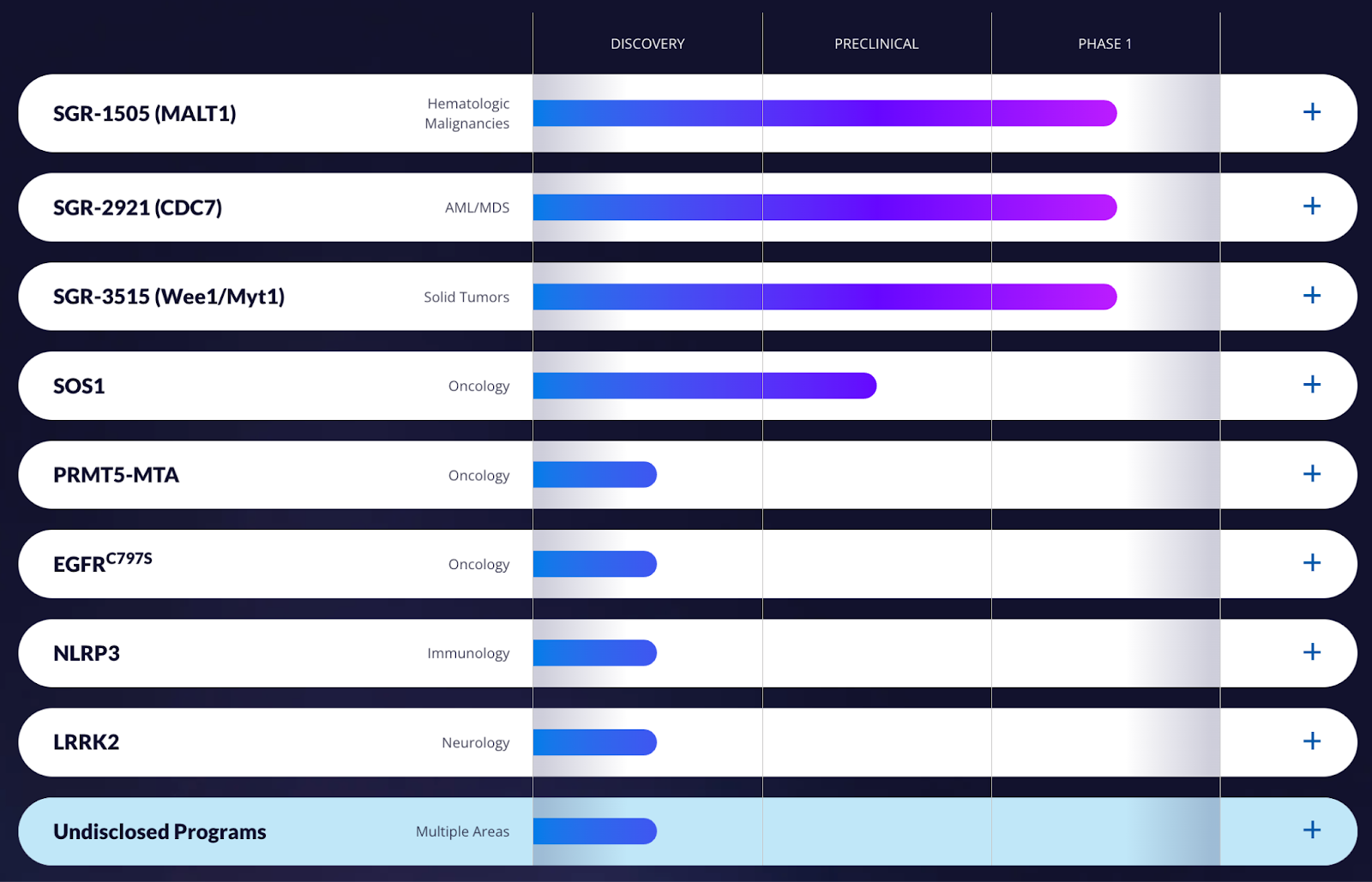

Schrödinger’s pipeline during its IPO roadshow vs. today, about five years later:

Source: Schrödinger S-1 filing (2020)

Source: Schrödinger’s website (2025)

Schrödinger’s materials science business, which has traditionally been a sideshow, has also begun to gain prominence.

In an equity research note titled “Materials no longer immaterial,” Bank of America analysts valued Schrödinger’s enterprise value (EV) at a tenfold multiple of its expected 2024 sales, “which is a premium to most names in the peer group, but reflects the additional long-term upside offered by the drug discovery business.”

Sherman said, “They have one phenomenal guy, this guy Mat Halls, who kind of came in and started building that business and he’s built it from scratch. You know, he could be the CEO of a materials spinout and I think that company would probably make ten times more revenue than they’re making right now.” Halls is currently listed as senior vice president of materials science.

“I think the battery stuff should be a separate business,” Despot agreed. “They seem a bit spread too thin.”

Despot explained his financial model and shared a price target of $110 per share in five years. If the businesses were separate, he estimated 50% of the value could be assigned to the software side, 30% to drug discovery, and 20% to materials science. “I think materials science is very interesting,” he said. “AI as well. My problem with them is that … it’s all under one umbrella, and so, are all these getting the right amount of attention?”

D’Cruz suggested that splitting up Schrödinger would potentially increase value. “Separately, the reliable, revenue-generating software business and the clinical-stage biotech business (with partnership income) would be valued higher,” he wrote to Hunterbrook.

The biotech investor who had recounted Farid’s dinner with Huang shared a similar perspective.

Farid disagreed in his interview with Hunterbrook, ascribing the success of the platform to the input of learnings from internal discovery and external partnerships.

The therapeutics would maybe be valued at negative EV, he said, at least until there was clinical data. “It’s nice for a biotech company to be able to generate revenue and not have to raise money every two years, and it’s really nice for a tech company to get that upside.”

“There are a lot of biotech companies trying to do what we’re doing and a lot of tech companies that are trying to do what we’re doing,” Farid pointed out. “23andMe tried that. Look what happened. Yesterday, they shut that whole thing down.”

The unified platform is also what Farid believes gives Schrödinger its edge in AI. “It’s all about the data. And there’s nobody else that can come even close to being able to generate the quality and the scale of data that’s required to make AI actually useful. Not even close.”

The tailwinds of AI

Schrödinger benefits from AI in three ways.

As innovation to produce more GPUs has reduced the cost of computation, the company’s ability to run AI and physics simulations has increased, accelerating the efficiency of its platform.

The protein structure prediction technology AlphaFold — for which Google’s DeepMind AI division won the 2024 Nobel Prize in Chemistry — has increased the universe of opportunities for Schrödinger’s platform.

And the integration of AI with Schrödinger’s physics-based platform has demonstrated enhanced results, including the creation of a new technology called machine-learned force fields, which more accurately and efficiently predict molecular properties.

D’Cruz said that Schrödinger has benefited from these advantages. “Schrödinger has invested significantly in AI/ML and developed applications to support their physics-based methods.”

Decreasing cost of compute

The growing hardware efficiency of GPUs should help Schrödinger reduce drug development costs and timelines. The more efficient computation becomes, the more firepower per dollar that Schrödinger and its clients can apply to drug discovery.

“Compute speed, cost per compute is definitely moving in the right direction,” said Sherman. “We’re already in a good place, and that’s just going to keep getting better and better.”

“We ran most things on CPUs at the beginning,” he recalled. “The GPU revolution was essentially like we got 100-fold speed-up almost overnight.” But, he noted, “These computations aren’t cheap. That’s something Schrödinger is struggling with. The pricing. If you look at the cost to run a calculation.”

“If it gets too much more expensive, you might as well just make the molecules,” he pointed out. This, he said, could undermine Schrödinger’s core value proposition of computationally iterating on the molecules before synthesis and testing in the real world.

David Cerutti, a GPU optimization engineer who used to be a senior scientist at Schrödinger, told Hunterbrook that GPU access had enabled Schrödinger to expand from targeted quantum mechanical products to its current suite of products.

Whereas a chemist might have synthesized a limited number of molecules a week in a traditional drug discovery program, Schrödinger was now enabling companies to model thousands of molecules per week.

Cerutti told Hunterbrook that the increasing availability of GPUs would likely lead to broader application of Schrödinger’s compute-intensive calculations — but also broader access from competitors developing open-source models for similar applications.

“It’s poised to be a pretty strong competitor to Schrödinger,” said Cerutti, speaking of a tool in development that he expects will be more affordable for many users.

Another former Schrödinger scientist was not concerned about potential competitors to Schrödinger’s platform. They texted that comparing a certain new computational design program to Schrödinger “is like comparing a Ford Taurus to a Ferrari.”

Sherman was also less concerned about open-source models and more concerned about market size.

“I don’t see Schrödinger’s business eroding so much as the question being how much is the market going to grow?” he asked. “Schrödinger’s got a pretty strong hold on the customer base partially because they just have accurate tools, partially because they have a rich, kind of complete ecosystem, and partially because they’re a big enough company that they have the sales, and they have the support, and they have all the professional stuff that comes along with being a big professional organization.”

Farid told Hunterbrook that he expects Schrödinger’s market to grow significantly. “You have this next kind of inflection that’s required,” he said. “The Novartis deal and the deal we did with Lilly are the beginning of that inflection.”

“That’s now what’s in the future is pharma companies really scaling up,” he concluded.

A growing universe of targets due to protein structure prediction

Schrödinger has also begun to benefit from tools like AlphaFold. It’s an AI model that predicts the three-dimensional structures of proteins based on their unidimensional protein sequence.

In October, DeepMind’s CEO Demis Hassabis and researcher John Michael Jumper shared half of a Nobel Prize in Chemistry for developing AlphaFold. Alphabet spun Isomorphic Labs out of DeepMind to apply its AI for drug discovery.

The other half of the Nobel Prize honored a similar technology developed by David Baker, a professor at University of Washington and co-founder of several startups. One of these, Xaira Therapeutics, debuted with $1 billion in April to use AI for drug discovery. In October, Baker’s lab also spun out Archon Biosciences, to pursue what industry publication Endpoints News called “an AI twist on antibodies.”

Getting a protein sequence is fairly straightforward. But until AlphaFold, predicting the structure into which that sequence would fold required challenging lab work. Expensive tools like x-ray crystallography and cryo-electromagnetic microscopy, or cryo-EM, each had limitations.

AlphaFold began to accurately predict many classes of protein structure and helped scientists solve many other structures for the first time, or with higher resolution than ever before.

One of Schrödinger’s tools, called a force field, predicts the motion of molecules. But there’s a challenge with using a force field to design medicines. You need a high-resolution structure of the protein that you’re designing the drug to target. Otherwise, the simulation is too fuzzy.

With only x-ray or cryo-EM, the targetable universe was restricted. Schrödinger had to turn away a lot of business from companies that wanted Schrödinger to help them target proteins for which Schrödinger’s force field wouldn’t be useful due to the lack of protein structure.

“SDGR management articulates their ability to overcome these issues through their physics based computational platform,” wrote a team of Goldman Sachs analysts in a September note titled “Schrödinger (SDGR): GenAI and broadening the lens for use cases of AI by biopharma.”

“Through physics, the company is able to produce and simulate data in silico (on par in quality with experimentation) for various molecular characteristics such as solubility and permeability, which can then be leveraged for machine learning.”

Now, thanks to AlphaFold, the universe of addressable targets for Schrödinger is multiplying, meaning more customers who can use its tools.

“AlphaFold is enabling for them, given that all these structures are becoming available,” said Despot, whose doctorate at MIT focused on systems biology and computational bioengineering.

Farid made an exception to his hesitancy to hype when it came to potential new targets.

“We have in our sights the ability to structurally enable every target in the human proteome,” he said.

“I think that’s going to surprise people: how quickly now the combination of cryo-EM, AlphaFold, IFD-MD, that’s one of the things that produces all the structures, AB-FEP, all this stuff can come together to structurally enable every target.”

“And boy, once you can do that, that’s going to have a big impact.”

Integration of AI with Schrödinger’s physics-based platform

Schrödinger also directly benefits from advances in machine learning algorithms that enhance its physics-based simulations.

Despot said “It’s more like optimization of the whole molecular dynamics modeling.” He also talked about Schrödinger’s application of AI for predictive toxicology, for which the Gates Foundation awarded a second, $9.5 million grant in November. “It’s something that’s definitely needed. … Preclinical discovery is like a real valley of death, and so if we can have this predictive toxicology and increase the efficiency, it could be a kind of true value creation.”

One of Schrödinger’s recent tools — AB-FEP+ (for absolute binding free energy perturbation) — provides accurate simulations, but at high cost. By training a type of AI called a convolutional neural network on the results of AB-FEP+ cycles, Schrödinger enables the AI to make similar predictions much more cheaply.

“Schrödinger’s development of free energy simulation methods, particularly FEP+, has been a significant value driver in drug discovery programs, both internally and through external collaborations,” Soumya Ray, a biotech entrepreneur who was previously a molecular modeler at Schrödinger, told Hunterbrook.

“This success has yet to be reflected in the company’s stock prices,” Ray added.

“A key reason may be that FEP provides optimal value only when deployed at scale,” he explained. “Unfortunately, Schrödinger’s current licensing structure for FEP is cost-prohibitive for most startups and mid-sized biotechs, making large-scale implementation difficult. In my view, this is a major factor limiting Schrödinger’s software sales, which could see greater returns with more flexible licensing models.”

He also speculated that one reason Farid hasn’t trumpeted AI is that many decision-makers still doubt its utility.

Despot said that when he speaks with Schrodinger, “You come with AI or machine learning questions, AlphaFold and everything, they get, not defensive, but they just don’t want to talk about it.”

Farid confirmed this in his interview with Hunterbrook. “There was a tremendous amount of hype around AI, and companies that were claiming they could do things that we knew they couldn’t do. And I overreacted to that,” he said. “I was basically saying, ‘This is so frustrating because it’s creating all this noise.’”

Jensen Huang pushed Schrödinger “to think bigger about what’s possible.”

Asher, of 1910 Genetics, believes that the technology is improving. “The opportunity for AI to revolutionize drug discovery has never been greater, has never felt more tangible,” she said. “And the reason why it feels so tangible this time around is because we’re finally grappling with the real barriers. We’re talking about AI in real terms of how do we overcome barriers in data, how do we overcome barriers in model, how do we overcome barriers in compute.”

“I respect Schrödinger for not jumping on the hype bandwagon of AI solving all problems in drug discovery,” said D’Cruz. “They have always been a high-science company that values solutions validated through extensive research. I do think that providing more information on how they are incorporating advances in AI/ML and their physics-based methods would be well received.”

The valuation challenge: software sales, biotech binaries, or something in between

In an industry notorious for expensive failures, biomedical companies have long hoped that AI would accelerate drug discovery, lower costs, and increase success rates.

With the exception of Schrödinger and a generation of smaller in silico companies (a moniker inspired by in vitro “in glass” test tube experiments or in vivo “in living” animal studies), many efforts to use computation stalled in the 1990s and early 2000s.

But around the time of Schrödinger’s IPO, the “techbio” sector, as biotech investor Vasudev Bailey dubbed it, began to break through.

Stanford University professor Daphne Koller raised hundreds of millions of dollars for her startup Insitro, which achieved a unicorn valuation while still in the earliest stages of preclinical development.

“All people care about right now is, ‘Show me your clinical data,’” said Asher, pointing out that “there is not yet an FDA-approved drug that could be described as AI-designed. … It’s more of a show-me-don’t-tell-me that your tech is great. Show me drugs that you have brought that have made a difference in patients’ lives.”

Recursion Pharmaceuticals (NASDAQ: $RXRX) topped $10 billion in market cap before publishing any clinical data, but now trades around $3 billion. It recently spent $688 million to acquire its longtime competitor Exscientia (NASDAQ: $EXAI), which had traded at over $3.5 billion before dismissing its CEO.

Despot highlighted the merger as a positive for the field. “Absolutely great. First of all, they were the two top companies in that kind of AI drug discovery. It’s a really complementary merger,” he said. “My bet is it’s going to be on the level of the Instagram/Facebook merger on the tech side.”

AbSci Corp. (NASDAQ: $ABSI), which develops biologic therapies rather than small molecules, also peaked at over $3 billion, but now trades around $300 million.

“The market has been very tough on some of these companies,” explained Despot.

“Schrodinger is moving steadily ahead, they’re not killing it. But on the other side, I do think that also there’s a bit of misunderstanding about what Schrödinger is actually doing.”

A long-time Schrödinger competitor, OpenEye, was acquired in 2022 for about $500 million by Cadence Design Systems Inc. (NASDAQ: $CDNS). Cadence disclosed that OpenEye would add about $40 million in 2023 revenue, less than a fifth of Schrödinger’s revenue that year.

Another competitor, Simulation Plus Inc. (NASDAQ: $SLP), has fallen more than 60% from its 2021 peak to around $600 million.

The current valuations of private companies in the sector — including the Chemical Computing Group (CCG), Atomwise, BenevolentAI, and InSilico Medicine, among many others — are not publicly disclosed but had ranged into the high hundreds of millions during the boom.

“Where are we for the Generation 1 companies?” asked Asher. “We’re not where we would’ve liked to be by now. Ten years in. Many, many billions of dollars invested.”

Despite the retrenchment of techbio, newer entrants like Genesis Therapeutics, Charm Therapeutics, and Chai Discovery have commanded high early-stage valuations.

“Do we actually need a Schrodinger?” Despot asked himself, referring to new AI companies entering the field. “Yes, we do.”

Unlike Schrödinger, most of these companies either sell and partner on software, or discover and develop drugs — not both. Schrödinger’s hybrid model has had a mixed impact on its perceived value.

Schrödinger’s in-house clinical pipeline: dead or alive?

Multiple biotech investors told Hunterbrook that while Schrödinger’s pipeline is “interesting,” they’re waiting on the company’s first clinical data from in-house drug development.

“We see upside from the underappreciated biotech pipeline,” wrote Jefferies in a research note. “SDGR’s ‘drug discovery’ pipeline of five cancer drugs is still in early stages, and most ‘HC generalists’ do not have the time or expertise to examine this closely. If software continues to do well and the ‘pipeline’ starts to show good data over the next 1-2 years, SDGR could move higher, given SMID-cap biotechs with even one blockbuster could trade to $2-5B with no software.”

Will Schrödinger publish results that turn one of their programs into an asset that could justify an entire company — like Morphic, Nimbus, Structure, and many other Schrödinger clients?

“It’s really hard for investors to figure out how to value a company with these two different business models. … It’s very difficult for a tech investor to understand biotech,” Farid told Hunterbrook. “And then of course, just as challenging actually, maybe a surmountable challenge but still a challenge is a biotech investor really understanding tech.”

Data on the horizon

Schrödinger’s first clinical data is expected in early 2025 for its molecule SGR-1505. The drug targets MALT1, a protein in a cascade of cellular communication known as the NF-κB signaling pathway. This cascade causes a class of lymphomas called non-Hodgkin’s B-cell lymphomas.

“The internal proprietary pipeline eg MALT1 etc is at $300M EV which we think is appropriate for a ‘small cap biotech’ peer group comp of preclin or Phase I type development stage,” wrote Jefferies following Schrödinger’s Q3 earnings, estimating the enterprise value of the program.

“Thus any upside from MALT1 or other assets is all upside and the MALT1 is the big catalyst here in our view,” Jefferies wrote, projecting that Schrödinger will present its data at the spring meeting of the American Society of Clinical Oncology (ASCO).

Clinical results from Schrödinger’s second and third programs are expected in the second half of 2025.

The second molecule, SGR-2921, targets a protein called CDC7 that regulates cell proliferation, which is linked to aberrant growth across many different types of cancer.

The third molecule, SGR-3515, targets a pair of proteins called Wee1 and Myt1.

Wee1, like CDC7, regulates cell proliferation. Myt1 is less well understood, but experiments show that the loss of both Wee1 and Myt1 kills cancer cells, a phenomenon known as “synthetic lethality.” Studies indicate that hitting Wee1/Myt1 could treat ovarian and uterine cancers.

“Can Wee1 be both alive and dead? Schrödinger hopes so,” wrote Jacob Plieth, a biotech journalist, referring to the hope that the target would work where others “have failed.”

His June 2024 article noted that Schrödinger’s SGR-3515 acts differently from failed Wee1 inhibitors developed by AstraZeneca Plc (NASDAQ: $AZN) and Zentalis Pharmaceuticals (NASDAQ: $ZNTL). Close behind Schrödinger’s program is another synthetic lethal Wee1 inhibitor from Acrivon Therapeutics (NASDAQ: $ACRV), which entered the clinic in the latter half of 2024.

Schrödinger’s preclinical programs include well-known targets like SOS1, linked to the infamous cancer-causing gene KRAS, and a specific mutation in EGFR, where earlier generations of EGFR-targeting drugs are the current standard of care for patients with advanced lung cancer.

Validated targets like SOS1 and EGFR are double-edged opportunities: Improving on an existing paradigm increases the odds of clinical success and means there’s an established commercial launch path but also entails taking on established competition.

Schrödinger is pursuing a more novel cancer target called PRMT5-MTA for tumors in places like the brain and central nervous system. An earlier program targeting the cancer protein HIF2 was returned to Schrödinger for its own development by its partner Bristol-Myers Squibb (NYSE: $BMY), which is continuing to work with Schrödinger on other oncology targets).

Schrödinger is also exploring targets validated for other types of diseases, like NLRP3 for inflammatory and autoimmune conditions, and LRRK2 for Parkinson’s, a program for which Schrödinger received research grants from The Michael J. Fox Foundation.

Goldman’s team summed it up in a 2024 analyst note: “The proprietary pipeline outlook continues to provide basis for anticipation and enthusiasm in our view.”

D’Cruz agreed, saying it was valid that part of Schrödinger’s conservative messaging may be because they’ve funded growth with revenue, rather than shareholder dilution.

“Looking ahead at the number of existing clinical programs and the ability to make progress rapidly on new programs, it is only a matter of time before significant value is unlocked via partnering,” he said.

Farid shared his former executive’s enthusiasm. “Is that going to be the beginning of an inflection? I think it is absolutely,” he said.

“All the signs are pointing in the right direction.”

Author

Nathaniel Horwitz is CEO of Hunterbrook and moonlights as a reporter. He was previously a venture partner at the healthcare investment firm RA Capital, where he co-founded, invested in, and served as a director on the board of companies ranging from AI-designed medicines for cancer to cell therapies for autoimmune diseases. He has a BA in Molecular Biology from Harvard. He has published in The Washington Post, The Boston Globe, The Daily Beast, The Atlantic, The Harvard Crimson, The New York Times, and The Australian Financial Review. His first job out of high school was reporting for his local paper.

Editors

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a BA in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life. Sam is based in New York.

Jim Impoco is the award-winning former editor-in-chief of Newsweek who returned the publication to print in 2014. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has a Master’s in Chinese and Japanese History from the University of California at Berkeley.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2025 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided "as is" without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.